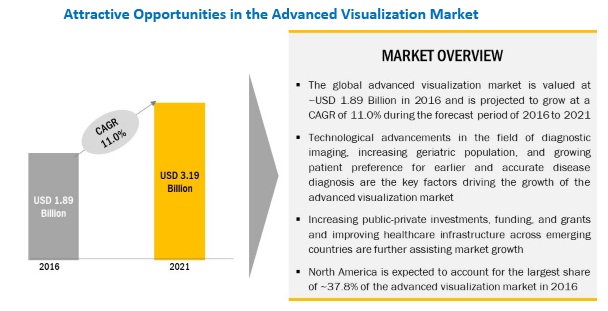

According to MarketsandMarkets, [182 Pages Report] The global advanced visualization market is projected to reach USD 17.07 billion by 2023 from USD 10.30 billion in 2018, at a CAGR of 10.6%.

Growth in the advanced visualization market can be attributed to factors such as technological advancements in the field of AV software, integration of AV software into PACS, improved diagnostic interpretation with AV tools, and development of novel AV solutions.

Driver- Advancements in AV software such as integration of PACs & AV tools

Product innovations in the AV market are mainly focused on the development of more cost-efficient technologically advanced and user-friendly software compared to the conventional ones. Advanced AV solutions simplify working with 2D, 3D, and 4D images obtained from various imaging modalities. These solutions are equipped with powerful and advanced communication features, cloud data handling (such as storage, post-processing, computing, and remote access); they also provide easy-to-use/automated workflow solutions to clinicians. Key vendors in the AV market are increasingly focusing on technological advancements and the launch of new AV software.

- From January 2012 to May 2016, the top 10 market players launched ~12 new AV systems in the global market. Such technological enhancements are stimulating the global demand for AV solutions.

- In September 2016, Vital Images Inc. collaborated with Nuance Communications Inc. for the integration of its PowerScribe 360 Reporting (a speech recognition technology for radiology) and PenRad Technologies, Inc. for its PenLung Lung Screening Management system (solution for radiology and imaging facilities to manage low-dose computed tomograph lung screening) into Vital’s Lung Screening solution.

- In November 2015, Vital Images, Inc. launched the CT Lung Screening Program solution, a radiology tool and workflow system for the standardization of lung nodules diagnosis and treatment plans.

Download a PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=111936030

A picture archiving and communication system (PACS) is a medical imaging technology for communicating diagnostic outcomes across healthcare systems. It is increasingly being integrated with other healthcare enterprise systems [such as image-enabled electronic health records (EHRs)/electronic medical records (EMRs), and health information systems (HIS)] to provide improved patient care. Most PACS vendors are now integrating AV solutions into their systems to provide advanced post-processing solutions for specialized applications. The AV functionality is integrated or embedded into PACS through a partnership between the PACS vendor and an AVIS (advanced visualization independent software) vendor. The integration enables healthcare providers to provide cost-effective solutions and streamline workflow efficiency of healthcare organizations. It also enables radiology departments to maximize their investments in PACS workstations and helps avoid delays such as relaunching or losing data as images are moved on machines. Thus, the integration of AV technology into PACS is expected to further stimulate the demand for AV software in the coming years. Some recent developments in this regard are listed below.

- In January 2016, Fujifilm Medical Systems U.S.A. Inc. received the FDA 510 (k) clearance for the marketing of Synapse 5, a PACS system that includes 3-D, vendor-neutral archive (VNA), radiology information system (RIS), cardiovascular, and mobile offerings.

- In November 2015, Philips Healthcare launched Lumify, a smart device ultrasound solution which allows portable diagnostic testing, connection with PACS, shared networks, and system directories through cloud-enabled technology.

- In September 2015, Philips received the FDA 510 (k) clearance for marketing of its Spectral Diagnostic Suite (SpDS), a set of advanced visualization and analysis tools that supports PACS.

Request a Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=111936030

Restraint- Limited availability of reimbursements for radiology-based diagnostic procedures

In 2006, the Centers for Medicare & Medicaid Services (CMS) announced an approximately 12 fold reduction on radiology remunerations. In line with the cost-containment and reduction strategies of the ACA, the agency proposed a rule in July 2014 which explains additional drops in the reimbursement for radiology practices.

Reimbursement changes for the technical part of imaging procedures (such as MRI and CT scans) is the most critical radiology billing problem. Several departments such as radiology, interventional radiology, and radiation oncology witnessed payment changes since 2015. The CMS provided updates about the changes in the reimbursement rates for specific Medicare services. Moreover, there was a decrease in the payment rate for many kinds of imaging procedures for radiologists, and this may impact finances in radiology departments. Thus, reimbursement cuts for radiology may hamper the demand for advanced visualization software as radiology accounts for a major share of ~54% in 2015.

Inquiry before Buying @ https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=111936030