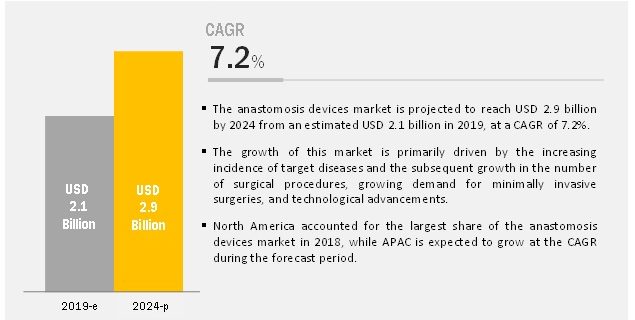

The global anastomosis device market is projected to reach USD 2.9 billion by 2024 from an estimated USD 2.1 billion in 2019, at a CAGR of 7.2% during the forecast period.

The growth of this market is primarily driven by the increasing incidence of target diseases and the subsequent growth in the number of surgical procedures, growing demand for minimally invasive surgeries, and technological advancements.

By type, the surgical staplers segment accounted for the largest share of the market in 2018.

Based on type, the anastomosis devices market is segmented into surgical staplers, surgical sutures, and surgical sealants & adhesives. Of all these segments, surgical staplers accounted for the largest share of the anastomosis devices market in 2018. The large share of this segment can be attributed to the advantages associated with surgical staplers (ease of use, minimal risk of complications, reduced blood loss/leakage, and shorter operating time) in comparison with surgical sutures and surgical sealants and adhesives.

Download a PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=5343963

By application, the gastrointestinal surgeries segment dominated the market in 2018.

Based on application, the market is segmented into gastrointestinal surgeries, cardiovascular & thoracic surgeries, and other applications. Gastrointestinal surgeries accounted for the largest share of the anastomosis devices market in 2018. The large share of this segment can be attributed to the rising incidence of gastrointestinal cancer and the extensive usage of anastomosis devices in these surgical procedures.

North America dominated the market in 2018.

In 2018, North America accounted for the largest share of the anastomosis devices market, followed by Europe. Factors such as the presence of advanced healthcare infrastructure in the region, increasing incidence of target diseases, growth in the number of cancer cases, increasing number of organ transplants, and the implementation of a new funding model for Canadian hospitals are contributing to the large share of North America.

Request a Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=5343963

Leading Companies

Johnson & Johnson (US), Medtronic plc (Ireland), B. Braun Melsungen AG (Germany), Smith & Nephew (UK), EndoEvolution LLC (US), CryoLife, Inc. (US), Becton, Dickinson and Company (US), CONMED Corporation (US), Intuitive Surgical, Inc. (US), Boston Scientific Corporation (US), Baxter International, Inc. (US), Péters Surgical (France), Biosintex (Romania), and Meril Life Sciences (India).