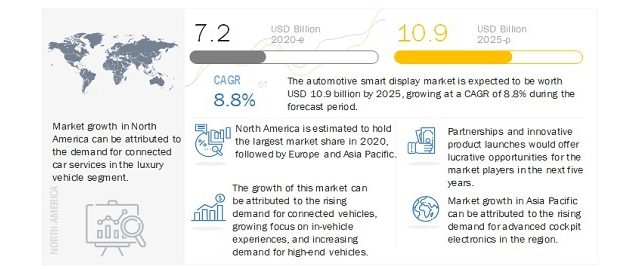

The Automotive Smart Display Market is estimated to be worth USD 7.2 billion in 2020 and is projected to reach USD 10.9 billion by 2025, at a CAGR of 8.8% during the forecast period. The market is driven by increased customer awareness about road and vehicle safety, demand for improved consumer experience in vehicles, and high growth in the luxury and high-end cars segments, mainly in the emerging markets.

Automotive smart displays help in two-way communication between a driver and a vehicle. Traditional automotive electronics included basic visual and analog interfaces, such as control buttons, analog and LCD instrument clusters, and basic central displays. However, modern automotive electronic components consist of multiple integrated advanced technologies that help create a seamless driving experience. Software providers play a vital role in the development of such advanced technologies. These providers help support the hardware part of these technologies by introducing innovative applications that support automobile manufacturers as well as OEMs to provide out of the box solutions to their customers. Some of the advanced automotive electronic components include advanced instrument clusters that are fully digital and/or 3-dimensional. Advanced center stack displays that integrate navigation and infotainment functions into a single screen platform, rear seat entertainment units, smart rear-view mirrors, gesture recognition solutions, and voice control, among others, are some of the applications of smart displays.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=25698331

The COVID-19 pandemic has presented an unprecedented challenge for the automotive smart display manufacturers as major OEMs partially or completely suspended vehicle production in major automotive markets. As the severity of the pandemic increases in Europe and North America, major automotive smart display manufacturers could lose significant chunks of revenue in 2020.

Europe is estimated to account for the largest market share by 2025, followed by North America and Asia Pacific. Technological advancements in current generation automotive cockpit electronics, along with the increasing trend of connected and autonomous vehicles, are further expected to drive the automotive smart display market. Increasing demand for a safe, efficient, and convenient driving experience; rising disposable income in emerging economies; and stringent safety regulations are also expected to contribute to the market growth. Increased production levels of automobiles, high adoption of advanced technologies in automotive electronics, and rapid progress of semi-autonomous and autonomous vehicles are also expected to boost the demand for automotive smart display in this region.

Passenger car segment is expected to be the largest automotive smart display market. A smart display system is required in a vehicle to enhance the functioning of cockpit electronics and safety features, among others. To cater to the high demand for safety, convenience, and comfort in the passenger car segment, advanced features are needed to be configured in the vehicles. OEMs are increasing the adoption of smart displays in the passenger car segment as a product differentiation strategy. The above-mentioned factors are expected to drive the automotive smart display market in the passenger car segment.

The luxury car segment is projected to be the fastest segment of the automotive smart display market during the forecast period. The leading vehicle manufacturers introduced their innovative and advanced features in this segment to stand out from the rest, which eventually fuels the growth of this segment. The growth of this segment can be attributed to the use of HUDs, which provide enhanced optical quality and increased brightness on a smaller display placed on the dashboard. This technology helps to meet compact space requirements, which in turn increases its adoption by OEMs.

Request Free Sample

Report @

https://www.marketsandmarkets.com/requestsampleNew.asp?id=25698331

Key Market Players:

Some of the leading manufacturers and suppliers of automotive smart display market is Bosch (Germany), Continental (Germany), DENSO (Japan), Visteon (US), Nippon Seiki (Japan), Panasonic (Japan), Pioneer (Japan), Yazaki (Japan), and others.

COVID-19 impact on automotive smart display market:

Major automotive smart display manufacturers such as Bosch, Continental, Panasonic, Denso, Nippon Seiki, Garmin, and LG Display have announced either suspension of production or adjustment of production due to the reduced demand and supply chain bottlenecks and to ensure the safety of their employees in China, Europe, and North America during the COVID-19 pandemic. For instance, COVID-19 has forced Continental to put a brake on its operations. As of April 2020, the increased outbreak of the virus has forced the company to temporarily cease production in more than 40% of its 249 production locations across the world. Visteon has taken decisive actions to manage costs and preserve liquidity, including effective cost management due to the COVID-19 pandemic. The company has temporarily suspended or reduced production at certain facilities in the Americas, Europe, and most of Asia outside of China in response to government requirements and lower demand for components due to production suspension by major OEMs. The company proposed a restructuring plan in January 2020 to reduce the number of employees at various sites to lower its cost base and improve financial performance. As a result of these developments, the demand for automotive smart displays is expected to decline in 2020. Manufacturers are likely to adjust production to prevent bottlenecks and plan production according to demand from OEMs and Tier I manufacturers. Major automotive smart display manufacturers lost revenues in Q1 2020. For instance, Garmin’s automotive segment recorded a revenue of USD 106 million compared to USD 127 million in Q1 2019. The Automotive segment revenue declined by 17% due to the ongoing Personal Navigation Devices (PND) market contraction and lower year-over-year OEM sales. In addition, the company has withdrawn its fiscal 2020 guidance due to the rapid and unpredictable economic changes caused by the COVID-19 pandemic. LG Display announced its Q1 2020 results in April 2020. Total revenue declined by 22%, from USD 5.0 billion in Q1 2019 to USD 3.9 billion in Q1 2020. Such declines are primarily caused by the COVID-19 pandemic. The company is projected to see a further decline in its revenue in the second quarter of 2020. Automotive smart display manufacturers are facing disruptions in supply chains as major countries are in a state of lockdown to prevent the spread of the disease. Thus, the market for automotive smart displays is projected to undergo a phase of decline in 2020.

To speak to our analyst for a discussion on the above findings, click Speak to Analyst