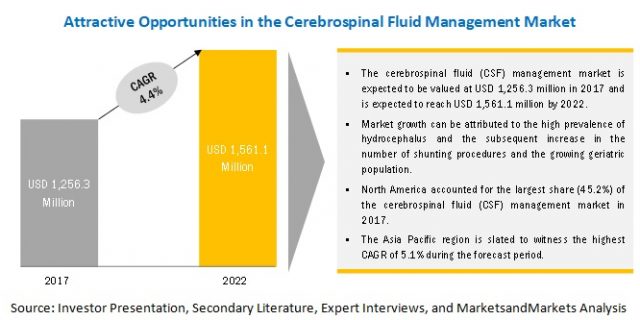

The global cerebrospinal fluid (CSF) management market is expected to reach USD 1.56 Billion by 2022 from USD 1.26 Billion in 2017, at a CAGR of 4.4%.

The key factors driving the growth of cerebrospinal fluid management market include the high prevalence of hydrocephalus and the subsequent increase in the number of shunting procedures and the growing geriatric population.

By product, the shunts segment held the largest share of the market in 2017

By product, the cerebrospinal fluid (CSF) management market is segmented into shunts and external drainage systems. In 2017, the shunts segment accounted for the largest share of the global market. The large share of this segment can be primarily attributed to growing number of shunting procedures performed worldwide as well as the increasing number of revision shunt surgeries owing to shunt malfunction and infection.

Download a PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=160672575

By end user, the pediatric segment accounted for the largest share of the market in 2017

On the basis of end user, the cerebrospinal fluid (CSF) management market is segmented into pediatric, adult, and geriatric end users. In 2017, the pediatric segment held the largest share of the global market. The large share of this segment can be primarily attributed to high prevalence of congenital hydrocephalus along with the rising number of shunting procedures in the pediatric population.

North America to dominate the market in 2017

In 2017, North America held the largest share of the cerebrospinal fluid management market, followed by Europe. Factors such as the rising prevalence of hydrocephalus, increasing funding for hydrocephalus research in the US, and the launch of Hydrocephalus Canada are contributing to the dominant share of this region.

Request a Sample Pages @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=160672575

Leading Companies

Medtronic (Ireland), Integra (US), B. Braun (Germany), DePuy Synthes (US), Spiegelberg GmbH & Co. KG (Germany), SOPHYSA (France), Natus Medical Incorporated (US), Dispomedica GmbH (Germany), Delta Surgical Limited (UK), Argi Grup (Turkey), Moller Medical GmbH (Germany), G. SURGIWEAR LTD. (India), and Wellong Instruments Co., Ltd. (Taiwan).