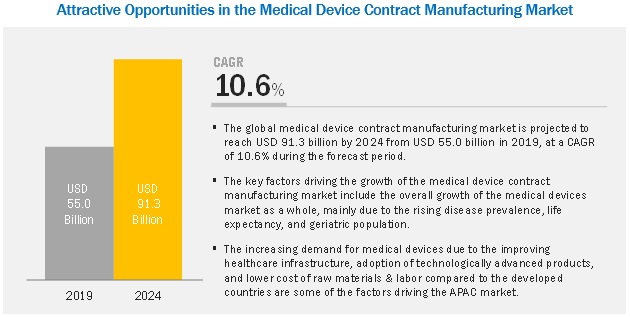

Market growth is largely driven by the rising global disease prevalence, life expectancy, and geriatric population. Technological advancements have prompted end users to overhaul or update their manufacturing systems. As this is a costly process, they look to contract manufacturing.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=170622851

According to research report the Medical Device Contract Manufacturing Market is expected to reach USD 91.3 billion by 2024 from an estimated USD 55.0 billion in 2019, at a CAGR of 10.6%.

Jabil Inc. (US) was the leader in the medical device contract manufacturing market in 2018. The company offers a focused range of products such as diagnostic devices, diabetes care devices, ophthalmology devices, pharmaceutical drug delivery devices, and consumables for medical devices and services such as additive manufacturing, contract manufacturing, quality management services, and final goods assembly services. It also offers advanced manufacturing technologies such as electronic manufacturing services and automation in a number of manufacturing facilities worldwide such as Singapore, Mexico, China, and the US, among others. The company also serves some of the top companies in other domains, such as Apple Inc., Cisco Systems Inc., Hewlett-Packard Company, Keysight Technologies, LM Ericsson Telephone Company, NetApp Inc., Nokia Networks, SolarEdge Technologies Inc., Valeo S.A., and Zebra Technologies Corporation that added to its brand recognition. Some of the key customers of the company for contract manufacturing services are Abaxis, Inc. (US), Ulthera, Inc. (US), and Antares Pharma Inc. (US). Jabil focuses on collaborating with the major pharma and medical device companies for contract manufacturing. For instance, in September 2018, the company collaborated with Johnson & Johnson for manufacturing medical devices.

Get report sample: https://www.marketsandmarkets.com/requestsampleNew.asp?id=170622851

•

On the basis of device type, cardiovascular devices and endoscopy

devices are both projected to witness the highest growth during the

forecast period between 2019 and 2024. The increasing prevalence of

cardiovascular diseases is expected to increase the demand for

cardiovascular devices in hospitals, diagnostic laboratories, and home

care settings. The volume growth of cardiovascular devices, coupled with

an increasing number of medical device companies opting for contract

manufacturing services in order to reduce the cost of manufacturing, is

expected to drive the market for cardiovascular devices during the

forecast period.

• By service, the final goods assembly services

segment is expected to witness the highest growth during the forecast

period. Market growth is largely driven by the increasing need for these

services by various OEMs, medical device companies, and pharmaceutical

companies that are involved in the manufacturing and sales of fully

integrated single-use medical devices.

• Based on the class of

device, the market is broadly segmented into Class I, Class II, and

Class III medical devices. The Class III medical devices segment is

expected to register the highest growth during the forecast period due

to the rising demand for pacemakers, implants, and ventilators. In

addition to this, the manufacturing of Class III devices requires

sophisticated and advanced technologies that can be a budgetary concern

for small and medium-sized medical device companies.