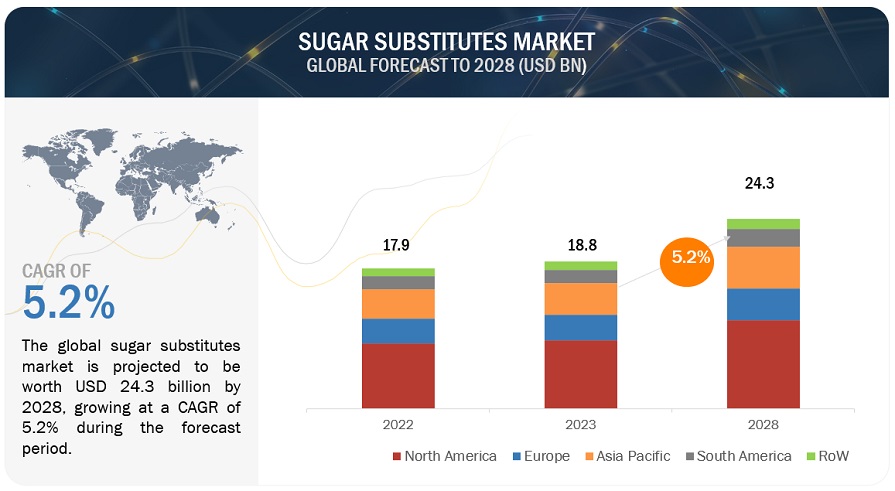

According to MarketsandMarkets “Sugar Substitutes Market by Type (High Fructose Syrup, High-Intensity Sweetener, Low-Intensity Sweetener), Composition, Application (Beverages, Food Products, and Health & Personal Care Products), and Region – Global Forecast to 2025″, the global sugar substitutes market size is estimated to be valued at USD 16.5 billion in 2020 and projected to reach USD 20.6 billion by 2025, recording a CAGR of 4.5% during the forecast period. The global sugar substitute industry has witnessed growing trends in the past years. The growth of this industry is majorly driven by an increase in health consciousness among consumers to encourage the demand for healthier food choices, an increase in demand for natural sweeteners due to the rise in consumer inclination toward natural products, and growing demand for sugar substitutes in various applications in the food & beverage industry.

Opportunities: Increase in investments in R&D activities by manufacturers to develope newer and enhanced products

Manufacturers are increasingly investing in the R&D of new sugar substitutes to gain a larger share than their competitors. Many food & beverage manufacturers are replacing regular sugars with sugar substitutes for lowering the calorie content of the final products. The demand for sugar substitutes from developed economies has increased. The major reason behind the substantial growth of the sugar substitutes market is the changing consumer attitude toward the consumption of sugar substitutes. The awareness about the ill-effects of high-calorie regular sugar consumption among consumers is increasing. To attract such potential consumers, sugar substitutes are made available across pharmacies, supermarkets, grocery stores, and health food shops in developed economies such as the US, Canada, and Germany.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1134

Challenges: Product labeling and trade issues

The international regulatory bodies for food safety and quality are making food safety regulations more stringent. Apart from food testing and certification, these international regulatory bodies are compelling manufacturers to follow food labeling rules and regulations. Governments of most nations are taking initiatives to implement the food labeling law in their country. For instance, Canada’s Consumer Packaging and Labelling Act and Regulations force manufacturers to follow labeling to fulfill purposes such as:

- Provide a uniform method of labeling and packaging consumer goods, overcoming the confusion of different requirements under other legislation

- Require full and factual label information from which consumers can make an informed choice in the marketplace

- Prevent misrepresentation and deception in packaging and labeling

- Require the use of metric units of measurement and bilingual labelling

The stringent regulations put by regulatory bodies about testing, certification, usage, production, and labeling pose a challenge for manufacturers.

By type, the high-intensity sweeteners segment is projected to experience the fastest growth in the sugar substitutes market during the forecast period

The high-intensity sweeteners segment is expected to experience the fastest growth in the global sugar substitutes market, on the basis of type, in 2019. The high-intensity sweeteners approved by the FDA are safe for the general population under certain conditions of use. Aspartame, sucralose, and saccharine are the major segments of the total high-intensity sweeteners market. Aspartame is the most commonly used low-calorie artificial sweetener in the highintensity sweeteners market. It is an odorless, white powder and is nearly 200 times sweeter than regular sugar. It is used as a food additive in desserts, sweets, drinks, chewing gums, and weight control products.

Make an Inquiry: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=1134

The North American region is projected to hold the largest market share during the forecast period

The North America region is projected to dominate the sugar substitutes market during the forecast period. The North American region is projected to dominate the global sugar substitutes market due to a variety of key factors, such as the busy lifestyle of consumers, increase in the prevalence of chronic diseases due to hectic lifestyles, and rise in awareness among consumers regarding the health benefits of reduced sugar in food and beverage products. The US has a large market for confectionery, bakery, packaged, and food convenience food products, due to which it constitutes a major share in the market. Consumers in the US are becoming calorie-conscious, attributed to the increase in health problems in the country. Due to these factors, low-calorie and low-fat food products are becoming popular in the country. The increase in incidences of obesity and cardiac diseases has led to a surge in demand for natural and low-calorie ingredient-based food products among consumers.

This report includes a study on the marketing and development strategies, along with the product portfolios of leading companies. It consists of profiles of leading companies, such as DuPont (US), ADM (US), Tate & Lyle (UK), Ingredion Incorporated (US), Cargill Incorporated (US), Roquette Frères (France), PureCircle Ltd (US), MacAndrews & Forbes Holdings Inc. (US), JK Sucralose Inc. (China), and Ajinomoto Co. Inc. (Japan).