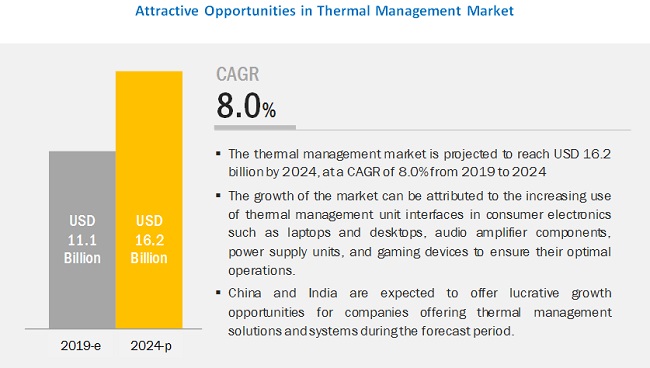

Thermal management market size was worth USD 11.1 billion in 2019 and is projected to reach USD 16.2 billion by 2024, at a CAGR of 8.0% during 2019–2024. Major drivers for the market are the rising demand for effective thermal management solutions and systems in consumer electronics; increasing use of electronic devices in different end-use industries; and ongoing radical miniaturization of electronic devices.

Download PDF Brochure @

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=155049228

The growth of the thermal management market is fueled by rising demand for effective thermal management solutions and systems for use in consumer electronics, increasing use of electronic devices in different end-use industries, and ongoing radical miniaturization of electronic. The growth of the thermal management market can also be attributed to the technological advancements such as the development of synthetic cooling systems and interface materials, the advent of cool chips for thermal management in electronic devices, and the increasing demand for natural refrigerants.

The market for nonadhesive thermal management material expected to hold the largest market share during the forecast period

The nonadhesive thermal management material segment is expected to lead the market between 2018 and 2024. Nonadhesive materials such as thermal pads, gap fillers, and grease are used widely in consumer electronics such as computers, laptops, and other handheld devices such as tablets. Thermal pads are used to fill the gaps between heat sinks and microprocessors. They eliminate air gaps to reduce thermal resistance and provide low-stress vibration dampening. Elastomeric pads were developed as an alternative to grease-based solutions used earlier for thermal management.

Advanced cooling devices expected to grow at the highest CAGR during the forecast period

The growth of this segment can be attributed to the increased adoption of microchannel cooling, cold plate cooling, and direct immersion cooling. The thermally conductive plates provide the most effective way to optimize liquid contact with hot surfaces as they enable the highest level of heat transfer due to the flow of liquid through layers of thermally conductive sheets. Direct immersion cooling is used widely in servers & data centers. In this process, servers are immersed in a nonreactive fluid or coolant for thermal cooling, thus eliminating the requirement for heat fans and heat sinks.

The market for optimization & post-sales support service accounted for the largest share in 2018

Optimization & post-sales support services are of critical importance in the thermal management market. There are two types of optimization methods that use active and passive thermal management solutions. Optimization & post-sales support services include maintenance and service offerings to reduce downtime of systems, elevate their overall performance levels, and maximize their operational life. They also include a choice of flexible service plans that can be customized according to the requirements of customers, extended product warranties, and comprehensive maintenance and repair plans. Optimization & post-sales support services are generally used as a critical quality control tool in servers & data centers as high temperatures can damage them and can result in loss of the vital information.

The market for consumer electronics expected to hold a major share of the thermal management market in 2018

Thermal management solutions are used prominently in several consumer electronics such as personal computers, laptops, smartphones, and gaming devices. Thermal management in consumer electronics involves chip cooling to protect electronic components such as processors and transistors from overheating. For multi-core processors, the noise can be avoided by using large heat sinks, heat pipes, and cooling fans. For instance, high conductivity materials such as phase change materials (PCMs) and thermal interface materials are used widely in smartphones and laptops to manage the cooling of electronic components and integrated chips. Thus, an increasing number of processors and the shrinking size of electronic components is leading to a rise in demand for thermal management solutions and systems in consumer electronics.

Asia Pacific held the largest share of the thermal management market in 2018

The region has emerged as a global focal point for large investments and business expansion opportunities. Moreover, increasing demand for effective thermal management solutions and systems from consumer electronics, automotive, defense, and healthcare sectors is also fueling the growth of the thermal management market in APAC. Flourishing chip manufacturing companies in countries such as China and South Korea are contributing to the growth of the thermal management market in APAC. The region holds a major position in the global semiconductor chip manufacturing industry with China, Japan, South Korea, and Taiwan.

The report profiles key players, including Honeywell International Inc. (US), Aavid Thermalloy LLC. (US), Vertiv Co. (US), European Thermodynamics Ltd. (UK), and Master Bond Inc. (US), Advanced Cooling Technologies, Inc. (US), Dau Thermal Solutions Inc. (US), Amerasia International Technology Inc. (US), Heatex AB (Sweden), and Parker Chomerics (US).