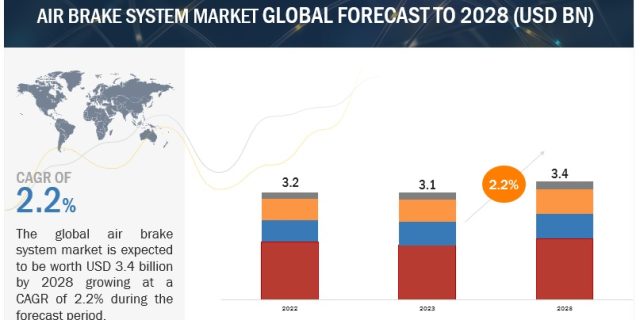

The global air brake system market size was valued at USD 3.1 billion in 2023 and is expected to reach USD 3.4 billion by 2028, at a CAGR of 2.2% during the forecast period 2023-2028. The air brake system market is expected to grow due to several factors. These include the rising demand for heavy commercial vehicles, the expansion of railways, increased long-haul transportation, and upcoming safety-related regulatory requirements. These factors will contribute to the increased adoption of air disc brakes in developed and developing countries.

“Heavy-duty truck to be the largest market for air brake systems”

Heavy-duty trucks include class 7 and class 8 trucks in which class 7 weighing approximately 12 to 14 tons, whereas class 8 trucks weighing upto approximately 15 t0 36 tons. According to OICA and MarketsandMarkets analysis, the production of heavy-duty trucks accounted for the maximum of the total truck production for all the regions, including North America, Asia Pacific, Rest of the World, and Europe in 2022 and is expected to dominate during the forecast period. Asia Pacific is the largest market for heavy duty trucks which contributes around ~59% of total heavy duty production at global level. Further, at global level production of heavy duty trucks is around 40% of total commercial vehicle production. Most heavy trucks have air brake systems due to their high load-carrying capacity. The main distinction between the air brake systems for rigid trucks and heavy-duty trucks lies in their load-carrying capacity and number of components. Fleet operators favor heavy-duty trucks for their strong weight-bearing capacity and engine power. The increasing development of economies in Asia and other regions is expected to drive the demand for heavy-duty trucks in the future. As a result, the heavy-duty truck segment is projected to be the largest market for air brake systems in terms of vehicle type.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=163805421

“Brake chamber is estimated to hold the largest market share in the on-highway air brake system during the forecast period.”

Brake chambers hold the largest market share in global air brake systems for on-highway vehicles. Air brake chambers are metallic containers situated at each wheel, which, when forced by compressed air, convert into mechanical force to stop the commercial vehicle. There are two kinds of air brake chambers, namely, service and spring brake chambers. A service brake chamber contains a flexible rubber disc called a diaphragm, a pushrod metal rod, and a return spring. When the brake pedal is pressed, compressed air fills the service brake chamber causing the brakes to apply.

As the brake chamber is placed at the end of the wheel, the number of axles decides the number of brake chambers in each commercial vehicle. Each axle has two brake chambers in a vehicle. Hence, the number of brake chambers increases with the GVWR of the commercial vehicle. The number of brake chambers in each vehicle may vary with each region, as the average number of axles in each region is different for heavy-duty vehicles and buses. North America and Europe have more multi-axle heavy trucks than Asia Oceania. Hence, the average number of brake chambers in buses in India is four, while in European countries, it is six. Asia Pacific holds the largest market share in the brake chamber market. The demand for brake chambers is related to the number of multi-axle commercial vehicles, as each axle requires two brake chambers. Further, growing commercial vehicle production will also drive the demand for the brake chamber market.

“Europe accounted for the second largest global air brake system market.”

Europe is estimated to be the second-largest market for air brake systems after Asia Pacific. Countries such as France, Germany, UK, and Spain have a higher production of commercial vehicles. The growth of air brake systems in Europe can be attributed to factors such as the growing production of heavy-duty trucks and stringent government regulations related to active safety. As per ACEB, road freight transport is a crucial way of trade and commerce in the European region. Trucks are responsible for >70% of freight transportation over the land in this region. As maximum transportation is conducted through these heavy trucks, it leads to fatal accidents in this region. According to European Union, out of total road fatalities in the EU in 2019, 14% and 2% died due to heavy good vehicle and bus crashes, respectively. Thus, the European Commission has implemented various braking system regulations for heavy commercial vehicles to avoid fatalities from heavy commercial vehicle crashes. For instance, European union mandates to install rollover stability control system in heavy trucks weighing above 3.5 tons.

Further, the inclusion of additional safety-related components to withstand the government braking-related mandates makes the price of the air brake system comparatively higher in Europe than in Asia-Oceania and North America. Additionally, Europe’s disc brake installation rate is the highest due to the shortest stopping braking distance for commercial vehicles. The above factors imply European commercial vehicles’ importance and safety standards. Thus, rising commercial vehicle production and adopting advanced technologies related to air brake systems by OEMs is anticipated to drive the growth of air brake systems in Europe.

Key Market Players

The air brake system market is primarily dominated by globally established players such as Knorr- Bremse AG (Germany),Meritor, Inc. (US), Haldex (Sweden), ZF Friedrichshafen AG (Germany), and Wabtec Corporation (US). These companies consistently develop new products, adopt expansion strategies, and undertake collaborations, partnerships, and mergers & acquisitions to gain traction across different regions in this air brake system market.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=163805421