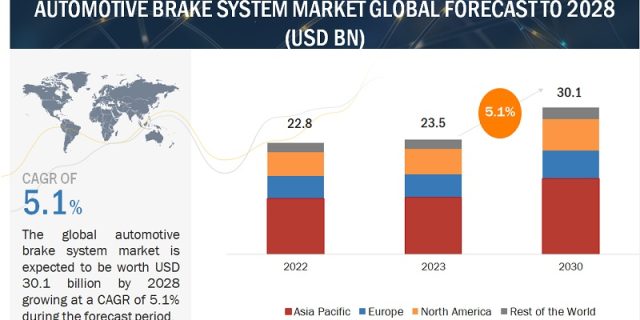

According to a research report “Automotive Brake System Market by Type (Disc, Drum), Technology (ABS, ESC, TCS, EBD, AEB), OHV Brakes (Hydraulic Wet, Hydrostatic, Dynamic), On & Off-Highway Vehicles & Electric Vehicles, Component, Actuation and Region – Global Forecast to 2028″ published by MarketsandMarkets, the automotive brake system market is projected to grow from an estimated USD 23.5 billion in 2023 to USD 30.1 billion by 2028 at a CAGR of 5.1% during the forecast period.

The automotive brake system market growth is mainly driven by the regulations on stopping distance and safety standards in countries such as China, India, Brazil, the European Union, the US, and Canada, among others. Further, growing demand for luxury cars worldwide and country-wise car assessment programs would boost the demand for electronic and disc brake systems. The growing adoption of disc brakes in heavy commercial vehicles, especially trucks, is another driving factor for the automotive brakes market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1070

Anti-lock Brake Systems (ABS) is the largest technology segment during the forecast period.

ABS will hold the largest share of the automotive electronic brake system market during the forecast period. Most governments have mandated ABS for light-duty or heavy-duty vehicles or both, considering the benefits offered by ABS. Also, according to the NHTSA, ABS is quite effective in non-fatal crashes, reducing the overall crash involvement rate by 6% in passenger cars and 8% in LCVs. For light-duty vehicles, ABS is already mandated in the US, Europe, Brazil, Japan, South Korea, and other countries. ABS penetration in Asia and other developing countries is comparatively lower; however, factors such as – OEMs’ focus on NCAP rating to showcase their product build quality and upcoming mandates emphasizing enhanced safety features – will direct the growth of ABS in light-duty vehicles.

Additionally, integrating anti-lock braking systems (ABS) in pneumatic brake systems for heavy commercial vehicles substantially enhances vehicle safety by preventing wheel lock-up and maintaining stability during braking and cornering. Some countries have set regulations compelling the installation of ABS in heavy commercial vehicles. For instance, in April 2019, the European Union (EU) mandated the inclusion of ABS and ESC systems in all new heavy-duty vehicles. Similar regulations are expected to be implemented in other countries. NHTSA’s updated regulation on mandating newly manufactured heavy truck tractors to achieve a 30% reduction in stopping distance is also expected to create a demand for ABS. All these factors are expected to drive the demand for Anti-lock Brake Systems in the coming years.

Disc Brakes will account for the largest and fastest-growing market by 2028.”

Disc brakes have gained popularity mainly in light-duty vehicles as they are more efficient, provide better stopping power, dissipate heat efficiently, self-adjust as the friction material wears, and work effectively in wet conditions. Today, most passenger cars and LCVs have disc brakes on the front wheels. The developing countries of Asia Pacific are dominated by economic cars equipped with disc brakes on the front wheels and drum brakes at the rear. This is mainly due to the lower speed limits and leniency in stopping distance in Asia Pacific countries. However, Class C & above are usually offered with all four disc brakes. Further, most of today’s passenger cars in Europe and North America are equipped with disc brakes on all four wheels as the demand for luxury vehicles is higher with higher power delivering higher speeds. Only some basic models have a disc brake on the front and drum brakes on the rear.

Alternatively, in heavy trucks and buses, disc brakes are growing steadily in Asia Pacific and North America as most vehicles are fitted with drum brakes. North American countries are gradually adapting the installation of disc brakes owing to increasing focus on safety and the stopping distance reduction mandate, along with disc brake installation government is making mandatory installation of Automatic Emergency Braking (AEB) System in heavy trucks. For instance, In June 2023, The U.S. Department of Transportation’s National Highway Traffic Safety Administration (NHTSA) and Federal Motor Carrier Safety Administration (FMCSA) announced a notice regarding the installation of automatic emergency braking systems for heavy trucks. On the other hand, Europe has a different trend as all the heavy commercial vehicles are equipped with disc brakes. This is mainly due to the stringent standards related to reduced stopping distance. Similar strict safety standards are expected to be implemented in countries such as China, India, Japan, and South Korea for medium and heavy commercial vehicles, which constitute major production of HCVs; disc brakes are likely to have increased usage in the Asia-Pacific and North America in the coming years.

The Asia Pacific will be the leading automotive brake system market over the forecast period.

The growth of the Asia Pacific automotive brake system market can be primarily attributed to upcoming advancements in automotive brake systems and expansions made by brake system manufacturers to cope with the increasing demand for disc brakes in passenger cars and light commercial vehicles. China, Japan, South Korea, and India dominate the Asia-Pacific automotive brake system market. Most of the cars sold in the Asia Pacific region are economy or mid-economy cars which are equipped with a disc and drum brake combination. Similarly, the majority of the heavy trucks in this region are equipped with drum brake systems. Hence, the drum brakes still have a good potential market in the Asia Pacific region. However, growing consumer preference from countries like China, Japan, India, and South Korea towards SUV cars with disc brakes will drive the demand for disc brakes.

Major countries such as China and India have a higher demand for economy & mid-range cars (including Class A, B, and C) contributing to nearly 50% and 90% in 2022. These cars are usually offered with 2 front disc brakes and 2 rear drum brakes. Further, to attract more consumers and showcase focus on enhanced safety, major regional automotive OEMs such as Toyota, Hyundai, Honda, and Suzuki have started offering all disc brakes with ABS in most of their newer Class C model cars. However, these markets are witnessing a growing demand for luxury and high-end cars that are installed with all 4-disc brakes for better stopping distance. These luxury cars are employed with advanced disc brake systems, thereby driving the disc brake market. For instance, the production of luxury cars in China has increased by 30% from 2020 to 2022. With the growing demand for luxury cars and high-end cars, the demand for premium disc brakes is anticipated to grow in the coming years.

In addition to this, Asia Pacific is the largest market for electric vehicles, especially in China. The growing sales of electric vehicles in countries such as Japan, China, and India will drive the demand for regenerative braking systems and disc brakes.

Key Market Players:

The automotive brake system market is dominated by globally established players such as Robert Bosch GmbH (Germany), ZF Friedrichshafen AG (Germany), Continental AG (Germany), AISIN Seiki Co, Ltd. (Japan), Knorr-Bremse AG (Germany), and Brembo S.p.A (Italy), ADVICS Co., Ltd. (Japan).

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=1070