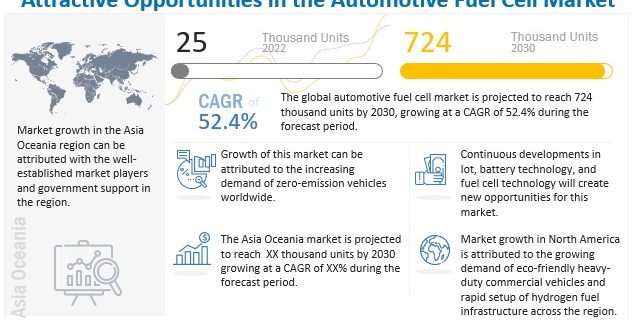

The global automotive fuel cell market is projected to grow from 25 thousand units in 2022 to 724 thousand units by 2030, registering a CAGR of 52.4%. Fuel cell operated vehicles such as buses, LCVs, passenger cars, and trucks, were mapped as part of this research.

The advantages of using FCEVs are zero emissions, high efficiency, more extended driving range than BEVs, less refueling time, and high efficiency in long-range transportation. Due to these advantages, several governments are investing in this technology, increasingly adopting fuel cell vehicles for public transport, and building the required hydrogen infrastructure. Fuel cell vehicles have better fuel economy and can travel around 300–400 miles on average with a full fuel tank. The refueling time for fuel cell-powered vehicles is around 3 to 5 minutes. This makes FCEVs an ideal way for transportation on definite or fixed routes. While the deployment of FCEVs is lower than PHEVs and BEVs due to their higher vehicle and fuel costs, several countries have announced ambitious targets for 2030, currently amounting to 2.5 million FCEVs.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14859789

The passenger car segment accounts for the largest share of the automotive fuel cell market by vehicle type. The rising demand for personal mobility and increased concerns for low emission vehicles are driving the sale of passenger cars. Several FCEV models are available in the market such as the Toyota Mirai, Honda Clarity, Mercedes Benz GLC FCEV, Nissan X-Trail FCEV, and Riversimple RASA. Realizing the significant potential in the fuel cell passenger car market, various companies are planning to launch new models in the coming years. For instance, BMW is planning to introduce the fuel cell technology developed together with Toyota in the BMW X6 and X7 models in the coming years. At the International Automobile Exhibition (IAA) 2019, BMW presented the i Hydrogen Next, a fuel cell study based on its X5 model. In September 2019, the company announced that a fleet of these vehicles is expected to be on the roads by 2022.

The fuel stack accounts for the largest share of the total cost of the fuel cell system. Platinum is used as a catalyst in a fuel stack to boost the electrochemical reaction and increase the efficiency of the fuel cell. Hence, the fuel stack segment is projected to lead the revenue from the automotive fuel cell market. However, in the coming time, platinum will gradually be used less as alternatives have been made for reducing the price of fuel cell stacks. Asia Oceania is estimated to be the largest market. Japan, China, and South Korea are the leading nations in fuel cell technology, and the adoption rate and growth of fuel cell technology are higher in these countries. Moreover, China is projected to lead the automotive fuel cell market by 2030. North America is projected to be the fastest growing region because of increasing investments by governments and adoption of fuel cell vehicles in the region. Europe has a growing market for fuel cell vehicles due to support for long-distance zero-emission transit. Companies like Ballard and PowerCell AB have been working on fuel cell stacks. For instance, in September 2020, Ballard Power Systems launched the high-power density fuel cell stack for vehicle propulsion, the FCgen HPS. It is a PEM fuel cell stack for medium and heavy-duty vehicles. In July 2022, PowerCell announced that they have partnered with ZeroAvia. Under which PowerCell will deliver 5000 units of 100-kW fuel cell stacks starting in 2024. Through these fuel cell stacks ZeroAvia intends to produce a 600-kilowatt, low-temperature, hydrogen-electric powertrain, that can be leveraged to power a 19-seat commercial aircraft.

Asia Oceania is projected to be the largest market by 2030. Increasing developments and investments, along with OEM push to popularize fuel cell vehicles, will boost the Asia Oceania automotive fuel cell market. North America is projected to be the fastest growing market due to increasing investments by governments across Europe and growing efforts to replace existing bus and taxi fleets with zero-emission vehicles. Europe will also be a large market, with the France and Germany working on low-emission vehicles for commercial transportation. Japanese OEMs like Toyota and Honda and South Korean OEMs like Hyundai are increasingly investing in boosting production capacities. For instance, Toyota is doubling its investments in fuel cell vehicles to expand production, thereby decreasing the cost of hydrogen fuel cell vehicles. South Korea is projected to be the largest market in Asia Oceania followed by China and Japan. India is expected to have the fastest growing rate followed by Australia. Currently, commercialization of hydrogen vehicles has just started in these countries. However, they will showcase huge opportunities in the coming time. Australia’s hydrogen energy as the hydrogen export could provide 2,800 jobs and add USD 1.2 billion annually to the country’s economy by 2030. The Government of Australia has announced to build a fuel cell manufacturing facility in the state of Queensland with an investment of USD 3.3 billion. It is also working with countries like Japan to develop its hydrogen-based capabilities.

Key Market Players:

The automotive fuel cell companies are Ballard Power Systems (Canada), Toyota Motor Corporation (Japan), Hyundai Group (South Korea), Hyster Yale (US), and Plug Power (US) among others.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=14859789