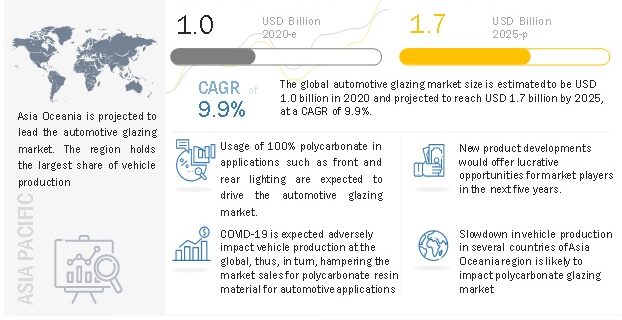

The global automotive glazing market size is estimated to be USD 1.0 billion in 2020 and is projected to reach USD 1.7 billion by 2025, at a CAGR of 9.9%. The market will be driven primarily because of the increase in demand for vehicle weight reduction owing to stringent emission norms. Polycarbonate weighs 50% less than glass and provides 20 times more strength which is estimated to drive the automotive glazing market for polycarbonate.

“Asia Oceania expected to be the largest automotive glazing market”

Asia Oceania is the largest automotive glazing market and is expected to retain its position during the forecast period. Asia Oceania has emerged as a hub for automotive production in recent years owing to increasing population and urbanization. According to OICA, Asia Oceania accounted for ~46% of the global vehicle production in 2018 because of the presence of OEMs such as SAIC, Hyundai, Toyota, Suzuki, Tata, and Honda. Manufacturers in this region are focused on developing specific solutions that address fuel efficiency mandates. As consumers in the region are showing an increased inclination toward convenience and safety, the region has witnessed higher growth than the matured markets of Europe and North America. Because of high vehicle production, the total market size is greater than North American and Europe because of which Asia Oceania is estimated to be the largest automotive glazing market.

Request Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=133207870

“Passenger car to be the largest market for automotive glazing, by vehicle type”

Passenger cars include vehicles such as hatchback, SUVs, and sedans. According to OICA, the production of passenger cars accounted for the maximum share of the total global vehicle production for all the regions including in 2020 and is expected to dominate during the forecast period. Due to the better adaptability to complex design and glass-like transparency, nearly all vehicles are equipped with polycarbonate front and rear lightings. Applications such as sunroof and rear quarter glass, which are used mainly in passenger cars, are estimated to have high potential for polycarbonate installation. With the increasing installation of sunroof and rear quarter glass applications in passenger cars and usage of polycarbonate for these applications, passenger car is estimated to be the largest segment by vehicle type.

“BEV is projected to be the fastest-growing automotive glazing market for electric vehicle”

Vehicle weight reduction is the predominant criteria in BEVs. As polycarbonate usage in glazing will reduce the vehicle weight by 20–25 kg, it will have a huge impact on the BEV range. Additionally, a majority of BEVs such as Tesla Model X, Model S, Model 3, and BMW i3 fall under the premium vehicle category Premium vehicles are equipped with sunroof and rear quarter glass. These applications are estimated to garner high potential for polycarbonate glazing. Increasing sales of BEVs coupled with the increasing penetration of polycarbonate glazing applications will result in BEV being the fastest-growing segment.

Inquire Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=133207870

Key Market Players:

Some of the key players in the automotive glazing market are SABIC (Suadi Arabia), Covestro AG (Germany), Teijin (Japan), Webasto SE (Germany), Trinseo (US), Mitsubishi (Japan), Chi Mei Corporation (Taiwan), Freeglass (Germany), KRD Sicherheitstechnik (Germany), and Idemitsu (Japan). SABIC and Covestro adopted the strategies of expansion, and new product development, to retain its leading position in the automotive glazing market.

Related Reports:

Automotive Windshield Market – Global Forecast to 2025

Automotive Glass Market – Global Forecast to 2027

Automotive Lighting Market – Global Forecast to 2027