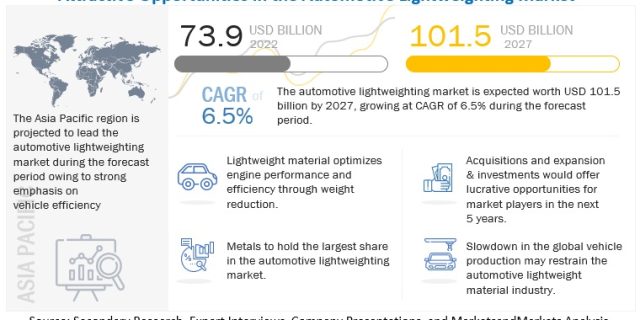

The automotive lightweighting market is projected to grow from USD 73.9 billion in 2022 to USD 101.5 billion by 2027, at a CAGR of 6.5% during the forecast period. Increasing demand of lightweight materials in the vehicles is due to increased safety components, incorporating batteries for extra mileage in electrical vehicles and government initiatives to reduce the CO2 and carbon footprints, are the driving factors for the Lightweight market.

Micromobility services are the most preferred services for the first and last mile transportation as they offer a convenient and cost-effective means of personal mobility. Micromobility vehicles are made of lightweight materials such as aluminum, plastics, elastomers, HSS, and others. These are mostly preferred materials while designing and manufacturing of the lightweight vehicles. Lightweight materials are a bit costly than conventional materials but can accommodate more safety features like sensors and extra battery storage for high range without increasing the weight and increase the load carrying capacity of the vehicle to increases the range of the vehicle to drive extra miles out of it. Most of the e-mopeds and e-bikes are made up of aluminum chassis as they are corrosion resistance, and it can be reused again after recycling. Aluminum tubes can be drawn in larger tube shapes so that it can accommodate many features and accessories in it without increasing the weight of the vehicle, which has generated more demand for such materials throughout the globe. With increased awareness and regulations, the scooter sharing concept has increased in European countries saving a lot of fuel by using micro-mobility vehicles, due to such awareness the demand for long range vehicles has increased globally, ultimately increasing the demand for lightweight materials. European government has generated guidelines for disposing old vehicles, to recover magnesium by recycling it again by reduced the demand for primary materials by 50%. Many key players like BASF SE (Germany), Covertro AG (Germany), and LyondellBasell (Netherlands) are investing in R&D for innovations. All these factors will boost the demand for incorporating the lightweight materials in the vehicles.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=23937731

Light weighting is done on many applications such as body in white, chassis & suspension, powertrain, closures, interiors, and others. In a vehicle nearly 85% of the weight is consumed by Body in white, chassis & suspension, and powertrain, hence many OEMs focus on these 3 parts for utilizing lightweight material and achieve maximum emission norms and regulations set by governing body. Alone BIW weighs 27% – 30% weight of entire vehicle, as they have to be welded with each other via spot welding process. By 2021, Europe region had mandated that cars should not emit more than 95g/km of CO2 and has set regulations by CAFE in US which will require lighter vehicles releasing 54.5 mpg of CO2 by 2025. These developments lead to the introduction of lightweight materials and innovative processes will enable manufacturers to meet these targets. On 25th August 2020, McLaren (England) introduced lightweight architecture for electrified supercars made in-house which cost them around USD 605,917.39 at McLaren Composites Technology Centre (MCTC) UK where they used carbon fiber composites mixed with resin that striped out excess mass for the BIW which increased the fuel economy.

The chassis and suspension contribute around 27% of total vehicle weight. According to US Department of Energy, they are targeting 35% weight reduction in chassis and suspension by 2025 and up to 55% by 2050. To which many OEMs shifted their concentration towards aluminum for achieving the targets. For the instance Audi (Germany) shifted to use hybrid aluminum for its A6 and A4 models, in areas like front and rear chassis legs, A-pillar, and the front section of the transmission tunnel. Considering all the developments and innovations to meet the norms and regulation set by governing bodies, has increased the demand for lightweight materials.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=23937731

Asia Pacific region is the largest market for Lightweighting Market.

Asia Pacific region has the highest market share and is expected to grow at higher pace due to strong demand in the automotive industry in countries like China, India, and others. The key driving factors for increased demand is fuel-efficient and less emitting vehicles. The country like China has abundant amount of raw materials at affordable cost which is a key factor driving the lightweight material in Asian market. According to primary APAC region has strong demand for passenger vehicles which has ultimately influence the automotive lightweighting market. Foreign OEMs have invested in Asia Pacific region, for instance Volkswagen Group (Germany), Mercedes (Germany), Ford (US), Renault (France) and others have built up their manufacturing units to fulfill the increased demand for fuel-efficient vehicles and stringent emission norms in Asia Pacific. Many OEMs are implementing the lightweight materials in their existing model or upgraded model, for instance Hyundai Sonata, 8th Generation hybrid model, that was introduced in 2019, which was 59 Kgs lighter than the previous generation model by using variable thickness over the walls of BIW panels using high strength steel and increased number of hot formed components. Ford (USA) had launched their Fusion in 2005 which weighted around 1.74 ton in those days whereas the new Ford fusion weighs only around 1.32 tons saving 0.4 tons using lightweight material in passenger car. All these factors have showcased more innovation and implementation of lightweight materials in Asia Pacific region compared to others.

Related Reports

All-terrain Vehicle Market – Global Forecast to 2028

Solar Vehicle Market – Global Forecast to 2030

Automotive Lightweighting Market – Global Forecast to 2027