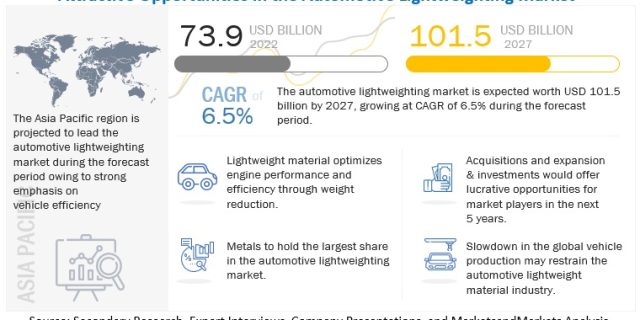

The automotive lightweighting market is projected to experience substantial growth, increasing from USD 73.9 billion in 2022 to USD 101.5 billion by 2027, with a CAGR of 6.5% during the same period.

The market report provides detailed insights into the automotive lightweighting market, including market data tables, figures, and an in-depth table of contents. It covers various aspects such as materials (metals, composites, plastics, elastomers), applications, components (frame, engine, exhaust, transmission, closure, interior), vehicle types (ICE, electric, micro-mobility, UAVs), and regional analysis.

The growth of the automotive lightweighting market can be attributed to the increasing stringency of emission regulations and the rising demand for fuel-efficient vehicles. Original Equipment Manufacturers (OEMs) are increasingly utilizing aluminum and carbon fiber materials to reduce the weight of vehicles. The growing demand for high-range electric vehicles is also a significant driver for lightweight materials. As electric vehicles become more prevalent, traditional components like fuel tanks and engines are being replaced by batteries and electronic components. This shift not only replaces conventional income sources but also creates new revenue opportunities for material suppliers.

Request Sample Report: https://www.marketsandmarkets.com/requestsampleNew.asp?id=23937731

The passenger cars segment is expected to hold the largest share in the automotive lightweighting market. Passenger cars offer extensive opportunities for employing lightweight materials in various applications such as interiors, body-in-white, and closures. A 10% reduction in vehicle weight can improve fuel economy by 6-8%, according to the Office of Energy Efficiency & Renewable Energy. Government bodies, such as the European Commission, have set stringent targets for reducing CO2 emissions from passenger cars, further driving the adoption of lightweight materials. High-strength steel, magnesium alloys, aluminum, carbon fiber, and composites are replacing conventional materials in passenger cars, leading to significant weight reduction. These lightweight materials are in high demand for components like frames, chassis, seats, and instrument panels in North America and the Asia Pacific regions.

Metals, including high-strength steel, aluminum, and magnesium alloys, dominate the automotive lightweighting market. These metals are used in chassis and wheel design. The usage of lightweight components in highly efficient engines can save billions of gallons of fuel annually. Plastics have also gained popularity in the automotive industry due to the incorporation of advanced features, which add weight to vehicles. Lightweight plastics are used in bumpers, exterior trims, and interiors.

Asia Pacific is expected to lead the automotive lightweighting market due to high vehicle production and increasingly stringent emission and fuel consumption regulations in countries like Japan, South Korea, India, and China. These regulations, along with the demand for comfort, safety, and luxury features, have increased the overall weight of vehicles. To counter this, OEMs are adopting lightweight materials. Safety regulations, such as mandatory airbag systems, also contribute to the demand for lightweight materials. The region shows a greater focus on low-cost plastics and lightweight metals, although there is an increasing demand for SUVs.

Inquire Before Buying: https://www.marketsandmarkets.com/Enquiry_Before_BuyingNew.asp?id=23937731

The automotive lightweighting market is dominated by key players such as BASF SE, Covestro AG, LyondellBasell Industries Holdings B.V., Toray Industries, Inc., ArcelorMittal, Thyssenkrupp AG, Novelis, Inc., Alcoa Corporation, Owens Corning, and Stratasys Ltd.

Related Reports:

Automotive Interior Market – Global Forecast to 2027

Automotive Paints Market – Global Forecast to 2025

Automotive Wheels Aftermarket – Global Forecast to 2027