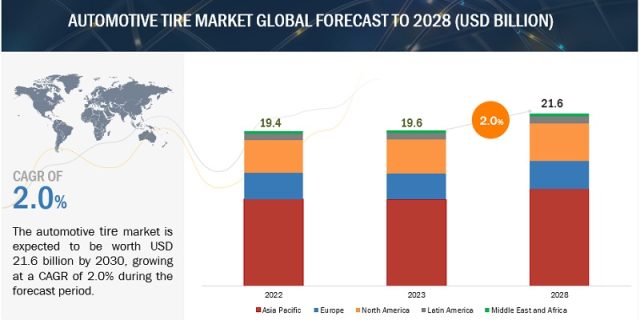

The Automotive tire market is estimated to grow from USD 19.6 billion in 2023 to USD 21.6 billion by 2028 at a CAGR of 2.0% over the forecast period. The key factors driving the automotive tire market are the vehicle’s increased life and the miles driven every year due to regular maintenance of the car, customer awareness, and advancement in new tire technology, which has led to longer life of the automotive tires.

The increasing demand for mid- & full-size SUVs and luxury cars will drive the automotive tires market. Also, the replacement market is primarily driven by the rising average life of vehicles and average annual miles traveled by light-duty vehicles. In the commercial vehicle sector, tire retreading significantly reduces operational costs by retreading tires, as tire expenses can be a considerable portion of their operational budget; tire retreading is a common practice for commercial and heavy-duty vehicles with high tire replacement costs. The retreading of the tire is mainly conducted on heavy-duty commercial vehicles (HCVs), such as trucks and buses, where the tire’s retreading extends the tire’s life by 50%. According to the Rubber Manufacturers Association (RMA), an HCV tire can be retreaded up to three times depending on the condition of the casing and the type of retreading process used. Considering the same, retreading tires can act as an opportunity for tire manufacturers.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=40166492

The passenger cars segment is dominating the automotive tire replacement market.

Passenger cars have a much higher ownership rate compared to other types of vehicles like commercial trucks and buses, due to which the segment is expected to lead the automotive tires market. According to des Constructeurs Automobiles (OICA), passenger car production in 2022 was around 61.5 million units. Also, the production of passenger cars accounted for ~70% of the entire vehicle production for the same year. Passenger cars come with various models, sizes, and styles, each with specific tire requirements to match their performance characteristics, hence a broad range of tire options in the market. Due to an increase in the average life of passenger cars due to technical advancements, the life of the passenger car park has also increased over a period of time. However, the higher average replacement life of tires brought on by technological advancements and the fluctuating cost of raw materials may limit the demand for tires in the aftermarket. According to Marklines and MarketsandMarkets analysis, there has been a shift in consumer preference from sedan vehicles to SUVs, where the market share for SUVs in passengers was ~49% in 2020 which grew to 53% in 2022 globally. This trend is expected to continue in the coming years. Increasing sales of SUVs will propel the demand for larger tire sizes (i.e., >15”) in coming years in OE and aftermarket.

Light commercial vehicles to witness significant growth in the tire retreading market.

Retreading of tires is mainly observed on heavy commercial vehicles (HCVs) globally. However, the retreaded tire offers benefits such as reduced waste, conserving resources, less energy usage (up to 70%) compared to manufacturing of new tire, etc. For instance, an average of 26 liters of petrochemical oil is consumed for manufacturing a single LCV tire which is just ~9 liters (almost 34%) of the new manufacturing process. This compensates for the rising raw material and labor costs, promoting the demand for these tires in the LCVs. According to the Retread Tire Association, the retreading of LCV tires costs ~USD 450–500 for four tires of large-size SUVs, and a new pair of tires for the same vehicle will cost ~USD 1,000, almost double the price. This is the key reason explaining the gradual growth in the demand for LCV tires retreading. Thus, many key players are majorly focused on retreading business for LCVs. For instance, JK Tires, on June 2019, opened its new retreading center in Pokhra (Nepal) for TBB, LCV, and PCR tires.

Asia Pacific is projected to be the fastest-growing OE and replacement market for automotive tires.

Asia-Pacific is considered the largest hub for manufacturing and sales of vehicles. According to Marklines and MarketsandMarkets analysis, this region contributes ~64% to global vehicle production and ~30% to global vehicle sales in 2022. Also, according to UN Comtrade, the Asia-Pacific region is the largest exporter of automotive tires globally, where China exports ~21% of automotive tires globally, followed by South Korea (~9%) and Japan (~6%). Secondly, the Asia-Pacific region contributed to ~39% of global vehicle parc in 2022, which makes it a more promising region for tire aftermarket. Many countries in the Asia-Pacific region have less stringent emission standards than other parts of the world, which has added older and polluting vehicles to remain on the road for a longer time. For instance, India announced a scrappage policy by the Ministry of Road Transport and Highways (MoRTH) in February 2021 for phasing out vehicles that are 15 years old for HCVs and 20 years old for passenger cars with the incentive of 4% of the vehicle’s ex-showroom price. Hence, due to such policies, the average life of the vehicle has increased more than the standard set life, which has increased the average replacement rate of the automotive tire. Hence these factors will drive the automotive tire market for OE and aftermarket in the Asia Pacific region.

Key Players

Prominent companies include Bridgestone Corporation (Japan), Continental AG (Germany), Goodyear Tire & Rubber Company (US), Michelin (France), and Pirelli & C. S.p.A (Italy) is the leading automotive tire manufacturer in the global market.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=40166492

Browse Related Reports:

OTR Tires Market – Global Forecast to 2027

Advanced Tires Market – Global Forecast to 2030

Connected Tires Market – Global Forecast to 2028