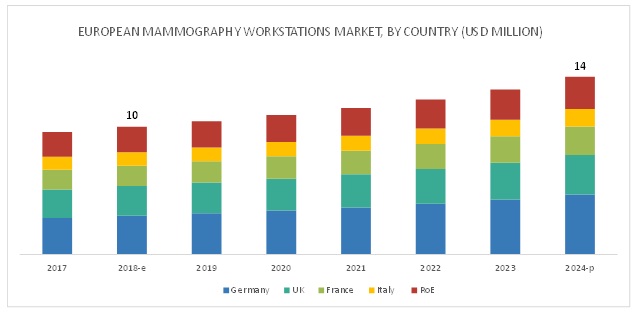

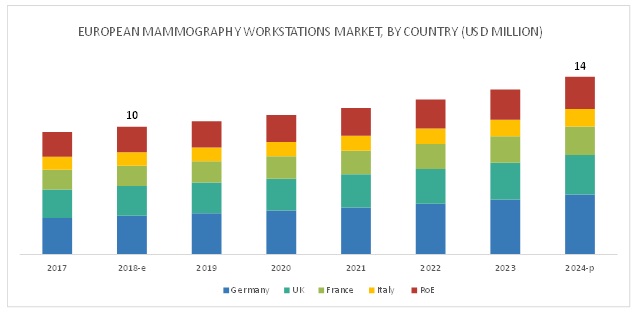

The Research Report on “European Mammography Workstations Market by Modality (Multimodal, Standalone), Application (Diagnosis, Advanced Imaging, Clinical Review), End User (Hospital, Breast Care Centers, Academia), Country (Germany, UK, France, Italy, Spain) – Forecast to 2024″, the mammography workstations market is projected to reach USD 14 million by 2024 from USD 10 million in 2018, at a CAGR of 5.5% during the forecast period.

Recent Developments;

– In February 2019, Fujifilm (Japan) launched ASPIRE Bellus II.

– In January 2018, Agfa-Gevaert NV (Belgium) signed a contract with the West Suffolk NHS Foundation Trust (UK) in order to implement enterprise imaging for radiology platform.

– In May 2017, Siemens AG (Germany) and Fraunhofer MEVIS (Germany) entered into a partnership for developing artificial intelligence software systems to facilitate diagnosis and therapy decisions in order to support physicians to define the best possible treatment approach.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=101392240

Industry Segmentation In Detailed:

The multimodality mammography workstations segment accounted for the largest share of the European mammography workstations market.

On the basis of modality, the mammography workstations market is segmented into mammography (X-ray) workstations and multimodality mammography workstations. In 2018, the multimodality mammography workstations segment accounted for the larger share of the European mammography workstations market. This can be attributed to the increasingly supportive government initiatives/regulations in Europe, increasing awareness about the diagnostic efficacy of contrast-enhanced digital mammography, growing market availability of integrated mammography solutions, techno-commercial advantages associated with multimodality mammography workstations, and the rising prevalence of breast cancer.

The breast care centers segment is expected to register the highest growth rate in the European mammography workstations market.

On the basis of end users, the mammography workstations market is segmented into hospitals, surgical clinics, & diagnostic imaging centers; breast care centers; and researchers & academia. The breast care centers segment is projected to witness the highest growth rate in the European mammography workstations market during the forecast period. This can be attributed to the increased utilization of multimodal diagnostic imaging (such as PET-CT, MRI, ultrasound, and mammography) in advanced breast cancer diagnosis, rising number of breast screening programs across major European countries, increasing number of training & awareness programs to sensitize healthcare professionals about the advantages of multimodality mammography workstations, and the growing number of public-private breast care centers across key European countries.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=101392240

Leading Key Players and Analysis:

General Electric (US), Siemens (Germany), FUJIFILM Corporation (Japan), Koninklijke Philips N.V. (Netherlands), Hologic Inc. (US), Carestream Health (US), EIZO Corporation (Japan), Agfa-Gevaert Group (Belgium), Barco (Belgium), Konica Minolta, Inc. (Japan), Benetec Advanced Medical Systems (Belgium), PLANMED OY (Finland), Sectra AB (Sweden), Aycan Medical Systems, LLC. (US), and Esaote SPA (Italy) are the major players in the European mammography workstations market.

Philips Healthcare (Netherlands) is among the top five players in the mammography workstations market. The company provides technologically advanced multimodal workstations for digital mammography, breast MRI, and breast ultrasound. To sustain its leading position and to further increase its share in the European mammography workstations market, the company focuses on introducing new products in the market. Philips Healthcare possesses a well-established supply chain network along with a strong network of raw material suppliers and product distributors in the Netherlands, Germany, the UK, France, Greece, and Italy. This reduces the company’s dependability on specific raw material suppliers or product dealers/distributors, which is an important market strength.

Geographical Analysis in Detailed:

The research report covers the European mammography workstations market across Germany, the UK, France, Italy, Spain, and RoE. Germany accounted for the largest share of this market in 2018. The large share of Germany is primarily attributed to the better reimbursement scenario in the country as compared to other European countries, wider acceptance of multimodality mammography workstations among major end users (such as hospitals, surgical clinics, and breast care centers), and the rising patient demand for improved cancer screening.

Speak to Analyst:https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=101392240