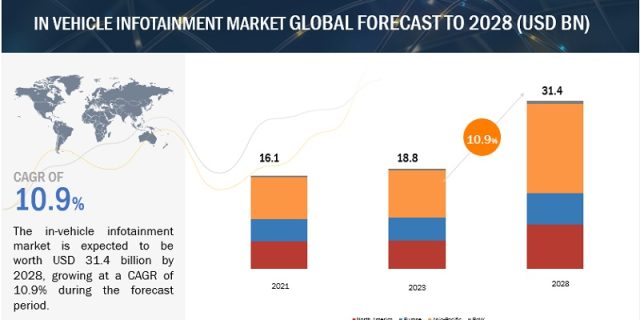

The in-vehicle infotainment market size is projected to grow from USD 16.4 billion in 2023 to USD 28.3 billion by 2028, at a CAGR of 11.6%. The in-vehicle Infotainment system aggregates all the vehicle’s infotainment functions, including tuner reception, media connectivity, audio playback, navigation, and HMI. It offers solutions such as audio/video entertainment and information content, including radio, media player, TV and video, telephony, navigation, speech control, apps, and connectivity features, which bring digital life right on the road. Asia-Pacific remains the key market for in-vehicle infotainment, though the demand is also substantial in Europe and North America.

Market Dynamics

DRIVER: Growth of the smartphone industry and use of cloud technologies

By the end of 2030, it is estimated that half of the total car cost will be dedicated to automotive electronics only. The growth drivers would be electronics and sensors, along with infotainment systems. According to study, smartphone sales were 4.4 billion units in 2017 and are expected to reach 6.6 billion units in 2022 and reach ~7.3 billion by 2025.

Further, the usage of Android-based smartphones has remarkably increased by 49.89% from 2017 to 2022. A similar trend is expected in the automotive sector because Android operating systems are one of the popular choices of most OEMs for mid-to-high-end car segments. The increase in sales of low-end cars has resulted in cost optimization of Android-based chipsets embedded in the infotainment system, thereby driving the Android OS market for automotive infotainment systems. Infotainment systems with advanced smartphone integration are trending in the automobile industry. Recently added to the list is the advanced technology available in Skoda Slavia. There is a choice of two advanced infotainment systems for the new Slavia. These allow smartphones to be paired via SmartLink technology and provide access to mobile online services. Both are operated entirely via the central color touchscreen, which measures 7 inches in the Active specification.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=538

OPPORTUNITY : Government mandates telematics and e-call services

Technologies such as telematics and in-vehicle infotainment are currently in their primary phase of development and deployment, and these technologies are expected to positively impact the safety and security of commuters in the future. The regulatory bodies are keen on imposing regulations to implement telematics solutions. Many developed, and developing countries such as the US, Brazil, Russia, and the EU have either launched or have planned to introduce telematics-related mandates for services such as emergency calls (e-call) and stolen vehicle tracking (SVT). Developing countries such as China and India also follow the trend of passenger safety and security laws, which will boost the market for telematics and infotainment solutions.

As mentioned, below table, governments of some countries have initiated mandatory safety measures in passenger vehicles, such as emergency assistance in case of accidents and e-calls, which include the vehicle making an emergency call to the state helpline and directing the precise GPS coordinates of the place where the accident has taken place.

Thus, implementing such government regulations for passenger cars and commercial vehicles to ensure the safety of drivers and passengers through features such as navigation, voice control, driver assistance, and other features is expected to offer growth opportunities in the in-vehicle infotainment market.

Android Automotive to register the fastest growth of all in-vehicle infotainment operating systems

Android is speculated to grow fastest during the forecast period. The adoption of Android OS is an open-source platform gaining traction due to its cost advantages, higher flexibility while developing programs, and increasing availability of services with a large user base worldwide. This platform offers a cost-effective solution compared to other systems, making implementing it more affordable. The development and commercialization of Android Automotive OS have attracted the attention of numerous automotive suppliers and original equipment manufacturers (OEMs). For example, prominent automakers such as General Motors and Stellantis have made significant announcements regarding adopting Google’s new Android operating system for powering infotainment systems across their entire vehicle lineup by the end of 2023. Also, Ford and Lincoln cars will switch to the same platform in two years, while others, including some Dodge models and the Lucid Air, use an Android-based system without Google Automotive Services. Collaborations between companies like Audi and Volvo with Google have resulted in the utilization of upgraded versions of infotainment systems. This widespread adoption indicates the growing prominence of Android OS and positions it as a key operating system for in-vehicle infotainment companies in the upcoming years.

Asia Pacific is estimated to be the dominant regional market.

Asia Pacific is projected to lead the global market for the in-vehicle infotainment market by 2028. The dominance is mainly due to the presence of countries with higher vehicle production in different segments. For instance, developing countries such as China, India, and Thailand produce most of the economy and mid-range cars; thereby showcasing a substantial deployment of affordable infotainment systems with some advanced features. On the other hand, Japan, China, and South Korea have higher adoption of medium to premium range vehicles which finds installation of more sophisticated infotainment technology that includes in-built navigation, voice command, high-resolution display, and other premium features. Further, this region’s countries have significantly improved internet infrastructure, spurring the demand for infotainment systems among the tech-savvy population to provide a more connected driving experience. Key manufacturers are focusing on entering strategic partnerships with market players for market expansion, R&D, and product advancement to keep up with the changing needs of passengers. For example, in 2023, Sibrose and Marelli Holdings Co., Ltd. announced their collaboration to provide advanced over-the-air solutions to the next-generation vehicle’s cockpit. This partnership aimed to enhance the functionality of the vehicle’s cockpit by leveraging Sibros’ advanced over-the-air software update and data management platform and Marelli’s expertise in automotive technology.

Key Market Players:

The in-vehicle Infotainment market is led by established players such as Harman International (US), Panasonic Corporation (Japan), Alps Alpine Co Ltd (Japan), Robert Bosch Gmbh (Germany), and Continental AG (Germany). These companies adopted several strategies to gain traction in this market.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=538