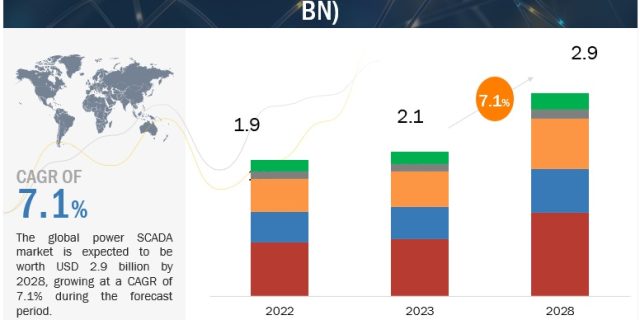

The global Power SCADA Market is expected to grow from an estimated USD 2.1 billion in 2023 to USD 2.9 billion by 2028, at a CAGR of 7.1% during the 2023–2028 period according to a new report by MarketsandMarkets™. Key to this growth is the increasing emphasis on the modernization and digitization of power infrastructure. Acknowledging the crucial role of SCADA systems, utilities and energy providers are driven by the pursuit of enhanced operational efficiency and reliability. The market is further propelled by the rising integration of renewable energy sources, such as solar and wind, into power grids, creating a demand surge for advanced SCADA solutions. Additionally, the complexity of power networks, necessitating real-time monitoring and control, contributes to the market’s expansion, with SCADA systems providing a centralized platform that effectively addresses this intricacy amid the proliferation of distributed energy resources, decentralized generation, and smart grid initiatives.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=36168289

Hardware segment to occupy majority of Power SCADA Market share.

The hardware segment, categorized by architecture, is anticipated to dominate the majority of the Power SCADA Market share for several compelling reasons. Firstly, hardware components form the foundational infrastructure of supervisory control and data acquisition (SCADA) systems, encompassing critical elements such as programmable logic controllers (PLCs), remote terminal units (RTUs), communication devices, and sensors. These components play a pivotal role in facilitating real-time monitoring, control, and data acquisition in power generation, transmission, and distribution processes. The intrinsic nature of power systems, characterized by the need for reliability, resilience, and high-performance functionalities, emphasizes the importance of robust hardware architecture. As organizations in the power sector increasingly prioritize the adoption of advanced and sophisticated SCADA solutions, the hardware segment becomes a focal point for investments. The demand for state-of-the-art hardware is particularly driven by the evolving complexity of power networks, the integration of smart grid technologies, and the requirement for seamless operations in the face of growing energy demands. Moreover, the hardware segment’s dominance is reinforced by the fact that many key players in the Power SCADA Market tend to manufacture complete SCADA systems in-house. This vertical integration allows these market players to exert more control over the supply chain, reducing reliance on external suppliers for critical components.

The remote terminal units (RTU) is expected to be the largest segment Power SCADA Market.

The Remote Terminal Units (RTU) segment is anticipated to be the largest market within the power SCADA landscape based on several factors that highlight the critical role of RTUs in supervisory control and data acquisition (SCADA) systems for power applications. RTUs serve as key data collection and control units, situated at remote sites within power networks. Their primary function involves interfacing with field devices, such as sensors and actuators, and transmitting data to the central SCADA system. Given the extensive coverage of power infrastructure, the widespread deployment of RTUs is essential for efficient and comprehensive monitoring and control. The increasing complexity of power networks, driven by factors like distributed energy resources, decentralized generation, and smart grid initiatives, amplifies the importance of RTUs. Moreover, the rising adoption of advanced technologies, including the Internet of Things (IoT) and smart devices, further enhances the significance of RTUs. As power systems become more interconnected and data-intensive, the demand for RTUs capable of handling diverse data sources and communication protocols increases. The need for increased automation and real-time responsiveness in power networks contributes to the prominence of RTUs. These units play a crucial role in enabling quick decision-making by transmitting timely data to the central system, facilitating efficient control of power generation, transmission, and distribution processes.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=36168289

Asia Pacific to emerge as the largest Power SCADA Industry.

Asia-Pacific is poised to emerge as the largest Power SCADA Market due to a confluence of factors propelling the region’s robust adoption of supervisory control and data acquisition (SCADA) systems in the power sector. Rapid industrialization, urbanization, and the continuous expansion of power infrastructure projects in countries such as China, India, Japan, and South Korea contribute to a soaring demand for advanced SCADA solutions. Governments in the region are actively promoting smart grid initiatives, emphasizing digital transformation, and investing heavily in upgrading power networks, thereby fueling the need for sophisticated SCADA systems for efficient monitoring and control. The presence of major economies with substantial technological capabilities, coupled with a proactive approach toward adopting advanced technologies, positions Asia-Pacific at the forefront of power SCADA adoption. Additionally, the increasing population and escalating energy consumption in the region further underscore the necessity for reliable and optimized power distribution, reinforcing the prevalence of power SCADA systems across diverse applications.

Key Market Players

Key players in the global Power SCADA Companies include ABB (Switzerland), Rockwell Automation (US), Siemens (Germany), Schneider Electric (France), and Emerson (US).