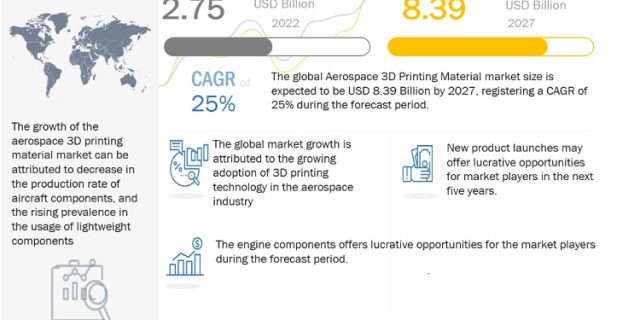

The global “Aerospace 3D Printing Materials Market By Material Type (Plastic, Metal, Others), By Printing Technology (DMLS, FDM, CLIP, SLA, SLS), By Platform (Aircraft, UAVs, Spacecraft), By Application (Prototyping, Tooling, Functional Parts), By End Product (Engine Components, Structural Components, Others), and Region – Global Forecast to 2027,” size is projected to grow from USD 2.75 billion in 2022 to USD 8.39 billion by 2027, at a CAGR of 25% during the forecast period. Increased demand for lightweight and durable aerospace components and simplification of complex designs will drive the growth of the aerospace 3d printing materials market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=41380192

Aerospace 3D printing materials are specifically engineered for the 3D printing of aerospace components. These materials are known for their strength, lightweight properties, and ability to endure extreme temperatures and pressures. Common materials include polymers like polyamide and polyetherimide, metals such as titanium and aluminum, and composites like carbon fiber-reinforced and glass fiber-reinforced polymers. They are utilized in the production of various aerospace components, including engine parts, airframe structures, and interior elements.

Aerospace 3d printing materials can be broadly classified into three major material types, namely, plastic, metal, and others. Various plastic materials that are used in the 3D printing include acrylonitrile butadiene styrene (ABS), polylactic acid (PLA), nylon, photopolymers, polyvinyl alcohol (PVA), polycarbonate (PC), high-density polyethylene (HDPE), and other thermoplastics.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=41380192

Based on product type, the aerospace 3d printing materials market is segmented into Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Stereolithography (SLA), and Selective Laser Sintering (SLS). FDM is a fast and efficient process for producing large volumes of continuous shapes in varying lengths with minimal waste. This process has a significant advantage in that it can produce complex shapes with varying thickness, textures, and colors.

On the basis of platform, the aerospace 3d printing materials market is segmented into aircraft, UAVs, and spacecraft. An aircraft would experience the greatest number of developments. The need for lightweight, cost-effective aircraft, as well as the need for rapid production of complex parts, would drive the use of 3D printers in aircraft manufacturing.

The various applications of aerospace 3d printing materials include prototyping, tooling, and functional parts. The advancements in 3D printing technology and the increasing adoption of 3D printers into manufacturing processes across industries can be attributed to the growth of the functional parts segment.

3D printing is used to develop various end products of aircrafts such as engine components, structural components, and others. Ease of design, improved strength, lightweight, and durability of manufactured components, as well as cost-effectiveness, all contribute to the growth of end products.

Request Customization: https://www.marketsandmarkets.com/requestCustomizationNew.asp?id=41380192

The US is the world’s largest aerospace manufacturing hub. One of the primary factors driving the overall growth of the market in the North American region is the increasing prevalence of 3D printing technologies for the manufacturing of complex and lightweight 3D components.

The major players in the aerospace 3d printing materials market includes 3D systems Corporation (US), Stratasys, Inc. (Israel), Materialise N.V (Belgium), EOS GmbH (Germany), Ultimaker B.V. (Netherlands), EnvisionTec GmbH (Germany), EXONE (US), General Electric (US) , Covestro AG (Germany), and Sandvik AB (Sweden).