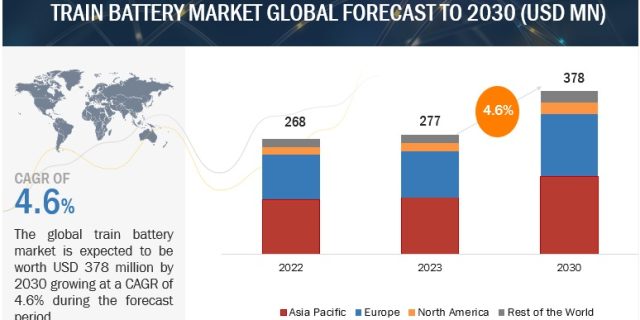

The train battery market is projected to grow from USD 277 million in 2023 to USD 378 million by 2030 at a CAGR of 4.6% during the forecast period. The train battery market growth is expected due to several factors, such as – the growing development of high-speed trains and metros and the expansion of railway networks. The rail sector’s emission regulations and high energy consumption remain major challenges. Energy storage systems such as batteries are expected to reduce the energy demand and thus reduce overall operational costs. These factors will contribute to the increased demand for train batteries in developed and developing countries.

The growth in the train battery market is primarily driven by factors such as development in the rail network, strengthening emission norms, and growing operating costs of the urban rail network, which are considered the most significant drivers of the train battery market. The rapid urbanization and growing need for sustainable transport are expected to lead to the demand for energy storage systems. They are expected to propel the demand for train batteries during the forecast period.

“Nickel-Cadmium batteries are expected to account for the largest share in 2023.”

During the forecast period, nickel-cadmium (NiCd) batteries hold the largest share in the train battery OE market. The growth of this market is mainly attributed to its increased usage in all types of rolling stocks. It offers many advantages, such as long cycle life, high current output, relatively low self-discharge rate, robustness, and durability. According to a whitepaper published by Saft, the life of NiCd would reduce about 20% for every 10°C rise in temperature. In comparison, the life of lead-acid batteries experiences a reduction of nearly 50% for the same every 10°C rise in temperature. Thus, due to its cost benefits, the usage of NiCd batteries is becoming increasingly popular in all types of locomotives, multiple units, light railways, trams, and passenger coaches, in addition to advanced trains such as metro trains and high-speed railways depending upon the application for the starter or auxiliary purpose. Owing to its benefits, as mentioned above, coupled with advancements in Ni-Cd technology to reduce the memory effect by the replacement of fundamental chemistry with nickel-metal hydride (Ni-MH) and nickel-zinc (Ni-Zn) batteries, these NiCd batteries resulted in higher reliability, efficient performance, and longer life. As the overall cost of ownership associated with owning a train battery is far higher than the initial acquisition cost, the railway operators are looking for a sustainable solution, due to which the market for NiCD batteries, especially sinter/PNE nickel-cadmium type, is expected to remain dominant in the coming years.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=6068646

“Electric Multiple Units is the largest engine head segment for train batteries during the forecast period.”

Electric Multiple Units (EMU) are estimated to be the largest and second fastest train battery market globally. The EMUs are installed with 1-2 batteries with a voltage requirement of 110V. The battery unit serves the purpose of both starter and auxiliary functions. EMUs have noticed a surge in demand owing to higher energy efficiency than Diesel Multiple Units (DMUs), helping reduce operating costs and meet stringent emissions standards. Further, the trend is moving towards high-speed EMUs, especially in countries like Japan, China, and the UK, as it offers quick and efficient point-to-point transportation. Several developments related to battery-operated EMUs and advanced battery technologies are expected to drive the market for train batteries. For instance, in June 2021, CAF was selected by the Rhine Ruhr Transport Association (VRR), and Westfalen-Lippe Local Transport (NWL) is considered as a preferred bidder for the contract to supply more than 60 battery-powered EMUs for Germany. Upcoming railway projects and expansion plans are expected to focus on electrified routes and intra-city transport. EMUs with high-speed capacity would have features like air conditioning coaches, automatic doors, train lighting, infotainment, Wi-Fi services, etc. Incorporating these systems would spur the demand for efficient energy storage systems, propelling the demand for train batteries in the EMUs.

“Europe is estimated to be the 2nd largest train battery market during the forecast period.”

Europe accounted for the 2nd largest global train battery market during the forecast period. Europe is the most developed region for adopting advanced battery solutions for different rolling stocks. Various countries from the European region are focusing on the electrification of existing railway lines due to stringent emission norms related to CO2. High fuel costs, large number of passengers, and strict emission norms are some of the primary factors that will drive the train battery demand in Europe as countries such as Germany, France, and Italy are investing heavily in the development of metros, light rails/trams, and hybrid locomotives.

According to the European Rail Research Advisory Council (ERRAC), in European metropolitan areas, 400 billion rail trips are made yearly: 15% by public transport, 30% by non-motorized means, and 55% by private cars. Rail represents 45% of the public transport. Furthermore, regarding rolling stock, EMUs account for approximately half of the total fleet, followed by passenger coaches and DMUs.

Nickel-cadmium batteries accounted for the largest share of the European train battery market across all rolling stock owing to high energy density and better performance at low temperatures compared to lead-acid batteries. However, the growing development in Lithium-ion battery chemistry such as lithium iron phosphate (LFP) & lithium titanate oxide (LTO) with high energy density and fire retardant characteristics and drawbacks of nickel-cadmium batteries such as high self-discharge rate compared to Lithium, driving the demand for lithium-ion batteries in European railway in advanced train segment. For instance, Hitachi, Bombardier, and Stadler are some of the manufacturers using lithium-ion batteries as traction batteries or auxiliary power backup batteries in their train models such as Hitachi Blues, Bombraider Talent 3, and Stadler FLIRT Akku.

According to the European Commission, as of 2021, 60% of the main lines rail network in Europe is electrified and around 80% of traffic is running on these lines, Belgium has the most electrified rail networks with ~87% out of total rail network. Further European countries are focusing on the development of fully battery-powered trains and hybrid trains for rail transportation. For instance, ABB Group formed a partnership with Stadler Rail to supply batteries for 160 trains in Europe and North America. ABB Group will provide traction as well as auxiliary batteries for these 160 trains which will be operated in Europe and North America.

The conversion of diesel engines with electro-diesel locomotives in the region has witnessed significant year-on-year growth. Governments of various European countries are constructing high-speed rail networks within and between countries for smooth transit. High-speed trains are one of the most used modes of transportation in Europe. High-speed trains such as Intercity Express, TGV, Eurocity, and Eurostar operate at approximately 250–300 km/h. The UK government has proposed a high-speed rail to connect London, Birmingham, Leeds, and Manchester. The project is estimated to cost USD 48 billion and is expected to be completed by 2026. The German government has proposed a high-speed rail project between cities such as Frankfurt–Mannheim, Karlsruhe–Basel, Hanau–Gelnhausen, Stuttgart–Wendlingen, and Wendlingen–Ulm. New high-speed lines are expected to increase the demand for high-speed trains, thereby increasing opportunities for train battery manufacturers. Further, SAFT, HOPPECKE Batterien GmbH & Co. KG, and Leclanché are some of the key players that serve the regional demand for train batteries of major locomotive giants such as Alstom and Seimens.

Key Market Players

The train battery market is dominated by players such as Saft (France), Enersys (US), Exide Industries (India),GS Yuasa Corporation (Japan), Amara Raja Batteries Ltd (India), and Hoppecke Batterien Gmbh & Co. Kg (Germany. These companies have developed new products, adopted expansion strategies, and undertaken collaborations, partnerships, and mergers & acquisitions to gain traction in the growing train battery market.

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=6068646