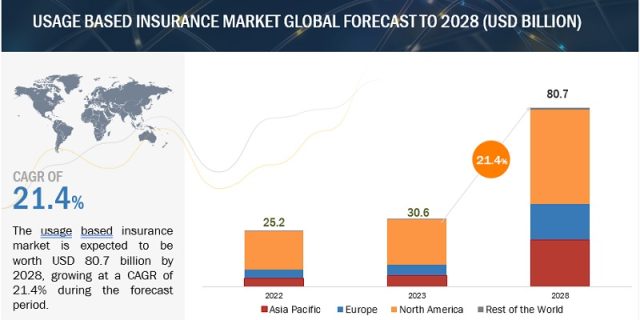

The usage-based insurance market is projected to grow from an estimated USD 30.6 billion in 2023 to reach USD 80.7 billion by 2028 at a CAGR of 21.4% during the forecast period.

The usage-based insurance market is estimated to be fueled by growing EV and ICE vehicle sales equipped with embedded telematic systems. These connected cars are equipped with multiple sensors that can gather data on driver behavior, mileage, speed, and braking patterns, making it easier for usage-based insurance companies to devise the premiums. Also, factors such as lower premiums and more personalized coverage are further expected to drive the market for usage-based insurance. Cutting-edge technologies such as AI, data science, and blockchain have been leveraged to lower insurance premiums compared to regular automotive insurance, which is also expected to drive the market.

Download PDF Brochure @ https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=154621760

Light Duty Vehicle (LDV) dominates the market by vehicle Type during the forecast period.

The scope defines Light duty vehicles as light commercial Vehicles (LCVs) and passenger cars. LDVs have more adoption of usage-based insurance as compared to HDVs. Connected passenger cars are more than connected commercial vehicles. Nowadays, most passenger cars are equipped with devices such as OBD-II embedded telematics systems or can be integrated with smartphones. This can gather all the information regarding driving habits and set the UBI plans. Furthermore, passenger cars are widely used – from daily commutes to occasional leisure trips. With the growing demand for ride-sharing and Mobility-as-a-Service, the need for UBI becomes more intrinsic.

The UBI service providers are developing new applications and services for connected cars, which can be used in parking and ride-sharing services. Also, the top key players are offering new UBI products and plan for light-duty vehicles, which are into ride-sharing, rental cars, personal use, and autonomous vehicles such as Drivewise, Drive Safe and Save, RightTrack, Snapshot, SmartRide, SafePilot, etc. Thus, the LDVs are expected to witness a substantial UBI penetration over the forecast period.

BEVs are the fastest-growing segment in the usage-based insurance market.

Battery electric vehicles (BEVs) are equipped with various sensors that generate data about vehicle usage, such as speed, mileage, braking patterns, and battery usage. Insurers can use this data to develop more sophisticated UBI programs that reward drivers for safe and efficient driving. BEVs are more predictable than gasoline-powered vehicles regarding their performance and maintenance needs. This makes it easier for insurers to price UBI premiums for BEVs. The BEVs help insurers attract and retain customers by offering UBI programs, especially to the younger drivers who are more likely to be interested in new technologies and personalized insurance products. According to the International Energy Agency, in 2022, SUVs and more oversized vehicles will dominate the available EV models. These vehicles contribute 60% of the total BEVs available in Europe, the US, and China. Also, according to Mark Lines, 6 million new BEVs and PHEVs were sold in the first two-quarters of global sales. Hence, these increased sales of BEVs in the US and Europe are driving the market for UBI.

The premiums for BEVs are also competitive compared to ICE vehicles, where automakers like Tesla (US) offer their own UBI program called “Safety Score,” which rewards Tesla drivers for safe driving habits, such as avoiding hard braking and accelerating. Tesla also uses vehicle data to give drivers insights into their driving behavior. Hence, these new initiatives by BEV manufacturers also drive the UBI market.

North America holds the largest market share for the usage-based insurance market.

North America has a high adoption rate of telematics, devices that collect data about vehicle usage. This data is essential for UBI programs, as it allows insurers to price premiums based on individual driving behavior. In addition, North American consumers are more aware of usage-based insurance, and the UBI acceptance is more in the NA region. Also, the North American insurance industry is quite competitive, where insurers seek innovative ways to attract and retain customers. UBI allows insurers to differentiate themselves and offer more tailored and competitive products.

The North American region holds a significant market share for the growing popularity of MaaS, driving demand for UBI programs. MaaS providers offer various transportation services, such as car sharing and ride-hailing. These services typically use telematics to track vehicle usage, which makes them ideal for UBI programs. OEMs and insurers are increasingly collaborating to offer UBI programs to their customers. For instance, GM and Progressive have partnered since 2015 and continue to provide a UBI program called “SmartDrive” to date. This program rewards GM drivers for safe driving habits, such as avoiding hard braking and speeding. North America has UBI’s top key players: Allstate Insurance Company, Farmers Insurance, Nationwide Mutual Insurance Company, Progressive Casualty Insurance Company, State Farm Mutual Automobile Insurance Company, etc.

Key Players

The UBI market is dominated by globally established players in North America, such as UnipolSai Assicurazioni S.p.A (Italy), Progressive Casualty Insurance Company (US), Allstate Insurance Company (US), State Farm Automobile Mutual Insurance Company (US), and Liberty Mutual Insurance Company (US).

Request Free Sample Report @ https://www.marketsandmarkets.com/requestsampleNew.asp?id=154621760