Research Methodologies Followed for This Study:

Primary Research:

In the primary research process, various sources from both the supply and demand sides were interviewed to obtain qualitative and quantitative information for this report. The primary sources from the supply side include industry experts such as CEOs, vice presidents, marketing & sales directors, technology & innovation directors, and related key executives from various key companies operating in the ATP assays market.

The primary sources from the demand side included experts such as technical experts. Primary research was conducted to validate the market segmentation, identify key players in the market, and gather insights on key industry trends and burning issues, and key market dynamics such as market drivers, challenges, and opportunities.

Secondary Research:

In the secondary research process, various secondary sources such as D&B Hoovers, Bloomberg Business, and Factiva have been referred to identify and collect information for this study. These secondary sources included annual reports, press releases & investor presentations of companies, white papers, certified publications, articles by recognized authors, gold standard & silver standard websites, regulatory bodies, and databases.

Download PDF Brochure@

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=223438780

Expected Surge in Revenue:

The global ATP assays market size is projected to reach USD 315 million by 2024 from USD 191 million in 2019, at a CAGR of 10.5%.

Major Growth Boosters:

Growth in this market is majorly driven by the increasing demand for ATP assays in pharmaceutical & biotechnology companies, rising investments in pharmaceutical & biotechnology R&D, the increasing prevalence of cancer and other chronic and infectious diseases, and the shift from culture-based tests to rapid tests.

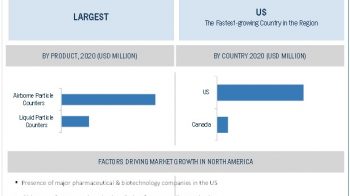

By end user, pharmaceutical & biotechnology companies accounted for the largest market share in 2018

Based on end user, the ATP assays market is segmented into pharmaceutical & biotechnology companies, the food & beverage industry, hospitals & diagnostic laboratories, and academic & research institutions. In 2018, the pharmaceutical & biotechnology companies segment accounted for the largest share of the market. ATP assays are emerging as preferred tools for screening potential drug compounds; therefore, many pharmaceutical and biotechnology companies are gradually replacing other in vitro and biochemical assays with cell-based assays, such as ATP assays, in drug discovery. Owing to the increasing adoption of cell-based assays, the use of ATP assay kits is also likely to increase in the coming years.

Key Questions Addressed in the Report:

# Which are the top 10 players operating in the ATP assays market?

# What are the drivers, restraints, opportunities, and challenges of the market?

# What are the prevailing industry trends, and what is the current scenario in the market?

# What are the growth trends in the market at the segmental and overall levels?

# How is the market performing in different regions across the globe?

Asia Pacific is expected to witness the highest growth in the ATP assays market from 2019 to 2024

The global ATP assays market is segmented into five major regions—North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. During the forecast period, the Asia Pacific market is estimated to grow at the highest CAGR, as several countries are witnessing a growing number of proteomics, genomics, and stem cell research activities, increasing research funding, rising investments by pharmaceutical & biotechnology companies, and the growing trend of research infrastructure modernization.

Request Sample Pages@

https://www.marketsandmarkets.com/requestsampleNew.asp?id=223438780

Global Leaders:

The prominent players in the global ATP assays market are Merck KGaA (Germany), Thermo Fisher Scientific, Inc. (US), PerkinElmer, Inc. (US), Lonza Group (Switzerland), Promega Corporation (US), Agilent Technologies, Inc. (US), Abcam plc. (UK), Danaher Corporation (US), Hygiena, LLC. (US), BioThema AB (Sweden), Abnova Corporation (Taiwan), AAT Bioquest (US), PromoCell GmbH (Germany), BioVision, Inc. (US), Geno Technology, Inc. (US), Biotium (US), Canvax Biotech S.L. (Spain), Creative Bioarray (US), Elabscience (US) and MBL International Corporation (US).