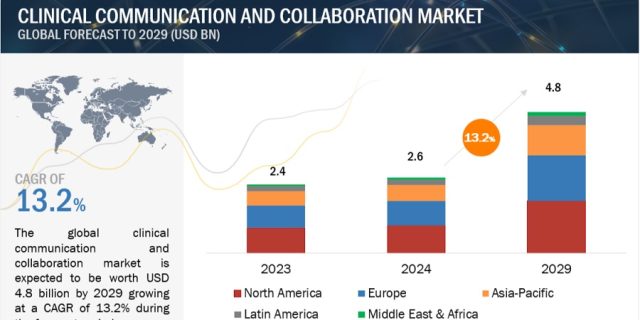

The global clinical communication and collaboration market is projected to grow rapidly from $2.6 billion in 2024 to $4.8 billion by 2029, at a compound annual growth rate (CAGR) of 13.2%. This growth is driven by several key factors, including the advantages of these solutions in enhancing patient care and safety, the significant demand for cost-containment solutions within healthcare delivery systems, the rising geriatric population, and the growing adoption of big data and mHealth tools.

Clinical communication solutions enable seamless flow of real-time health data, enabling constant patient monitoring, minimizing errors, and ensuring timely interventions, ultimately enhancing patient safety and care quality. However, the high investments required to build and maintain robust IT infrastructure pose a significant restraint for some healthcare providers, particularly smaller clinics with limited budgets.

Download a PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=118830286

The growing adoption of Electronic Health Records (EHRs) presents a significant opportunity for the market, as the integration of clinical communication and collaboration solutions with EHRs can enhance communication efficiency, facilitate seamless information exchange, and support coordinated care efforts. However, data security issues remain a challenge, as healthcare organizations grapple with safeguarding sensitive patient information while enabling efficient communication among care teams.

The market is segmented by platform, component, deployment mode, application, end-user, and region. The software component accounted for the largest market share in 2023, driven by the increasing adoption of digitalization and technological advancements in the healthcare sector. The cloud-based deployment model is expected to register the highest growth during the forecast period, offering enhanced accessibility, mobility, scalability, and cost-effectiveness.

Hospitals and clinics dominated the end-user segment in 2023, attributing to the increased adoption of software solutions for enhanced patient care. Geographically, North America accounted for the largest market share in 2023, while the Asia-Pacific region is expected to grow at the highest CAGR during the forecast period, driven by a rapidly expanding healthcare landscape, rising chronic disease prevalence, and increasing investments in digital health infrastructure.

Prominent players in the market include Avaya LLC, Oracle, Cisco Systems, Inc., Microsoft Corporation, Baxter International (Hillrom), symplr, NEC Corporation, Spok Inc., Vocera Communications (Stryker), Ascom Holding AG, Everbridge, Hidden Brains InfoTech, Imprivata, Inc., CommuniCare Technology, Inc. d/b/a Pulsara, Mobile Heartbeat (C-HCA, Inc.), OnPage, HARRIS ONPOINT, Jive Software, LLC, TigerConnect, JCT Healthcare Pty Ltd., Amplion, AndorHealth, PerfectServe, Inc., QliqSOFT, Inc., and Connexall, GlobeStar Systems Inc.