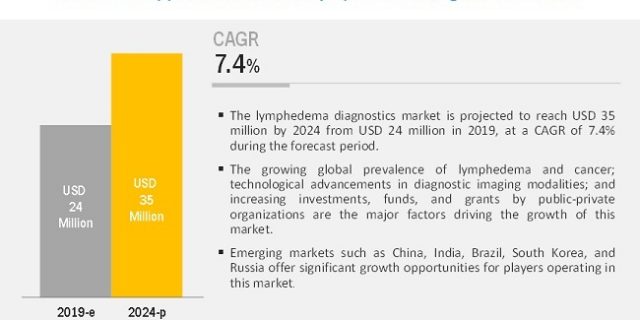

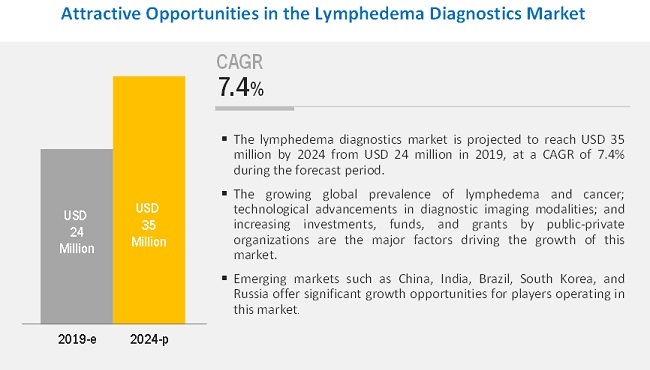

The Research Report on “Lymphedema Diagnostics Market by Technology (Lymphoscintigraphy, MRI, Near IR Fluorescence Imaging, Ultrasound), Disease Type (Cancer, Inflammatory Diseases, Cardiovascular, Filariasis), End User (Hospitals, Diagnostic Centers) – Global Forecasts to 2024″, is projected to reach USD 35 million by 2024 from USD 24 million in 2019, at a CAGR of 7.4%

Market Size Estimation;

Both top-down and bottom-up approaches were used to estimate and validate the total size of the lymphedema diagnostics market. These methods were also used extensively to estimate the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

- The key players in the industry and markets have been identified through extensive secondary research.

- The industry’s supply chain and market size, in terms of value, have been determined through primary and secondary research processes.

- All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources.

Data Triangulation;

After arriving at the overall market size—using the market size estimation processes as explained above—the market was split into several segments and subsegments. In order to complete the overall market engineering process and arrive at the exact statistics of each market segment and subsegment, data triangulation and market breakdown procedures were employed, wherever applicable. The data was triangulated by studying various factors and trends from both the demand and supply sides in the market.

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=145177203

Industry Segmentation In Detailed:

The lymphoscintigraphy segment accounted for the largest share of the lymphedema diagnostics market in 2018.

Based on technology, segmented into lymphoscintigraphy, magnetic resonance imaging (MRI), ultrasound imaging, computed tomography (CT), X-ray lymphography, bioimpedance analysis, and near-infrared fluorescence imaging. In 2018, the lymphoscintigraphy segment accounted for the largest share of the lymphedema diagnostics market. The noninvasive nature and easy reproducibility of this technology, and the fact that lymphoscintigraphy does not adversely affect the lymphatic vascular endothelium are some of the key advantages supporting the adoption of this technology.

The cancer segment accounted for the largest share of the lymphedema diagnostics market in 2018.

On the basis of disease type, segmented into cancer, inflammatory diseases, cardiovascular disease, and other diseases (congenital abnormalities, trauma-related conditions, infections, and filariasis). The cancer segment accounted for the largest share of the lymphedema diagnostics market in 2018. The large share of this segment can be attributed to the rising prevalence of cancer-associated lymphedema and increasing awareness about early disease diagnosis.

Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=145177203

Leading Key Players and Analysis:

The major players operating in the lymphedema diagnostics therapy market are GE Healthcare (US), Philips (Netherlands), and Siemens Healthineers (Germany). Other prominent players in this market include Canon, Inc. (Japan), Shimadzu Corporation (Japan), Stryker Corporation (US), Fluoptics (France), United Imaging Healthcare Co., Ltd. (China), Hitachi, Ltd. (Japan), Esaote, SpA (Italy), Neusoft Corporation (China), Mindray Medical International, Ltd. (China), Mitaka USA, Inc. (US), Curadel, LLC (US), and ImpediMed Ltd. (Australia).

GE Healthcare (US) is one of the leading players in the global lymphedema diagnostics market. To sustain its leadership position and ensure its future growth, the company has been focusing on product launches and agreements, partnerships, and collaborations as its key strategies. The company has also been focusing on geographic expansions and the development of low-cost equipment specifically for developing nations. For instance, in May 2017, the company collaborated with the Government of Egypt to supply a wide range of technologies and train doctors, nurses, and technicians about advanced imaging systems in over 200 Egyptian hospitals. With a wide product portfolio and strong geographic presence, the company is expected to witness significant growth in the lymphedema diagnostics market in the coming years.

Geographical Analysis in Detailed:

The lymphedema diagnostics therapy market is segmented into four regional segments, namely, North America, Europe, the Asia Pacific, and the Rest of the World. The large share of North America can be attributed to factors such as the easy availability and rapid adoption of technologically advanced imaging systems; high incidence/prevalence of lymphedema; and the strong, well-established healthcare systems. The market in the Asia Pacific is expected to grow at the highest rate, followed by Europe.

Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=145177203